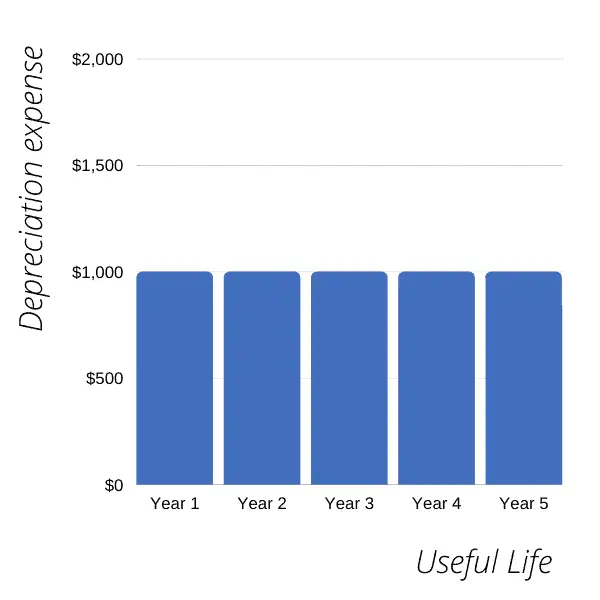

Under the straight line method, the depreciation expense is evenly distributed over the asset’s life.

If we plot the depreciation expense of an asset with a depreciable cost of $5000 and 5 years of useful life using the straight line method, it will look something like this:

Notice that this graph shows the depreciation expense over an asset’s useful life and not the accounting years, which are rarely the same.

The graph of depreciation expense calculated using the straight line method will always look like the one above if the asset’s useful life coincides with the accounting year.

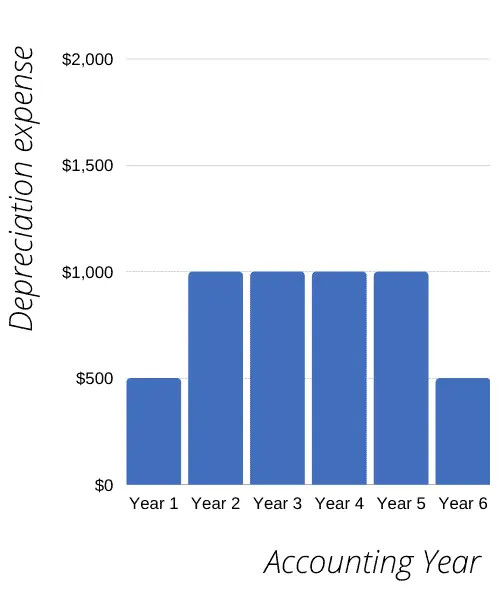

However, because the assets are usually purchased and sold sometime during an accounting year rather than on the first and last days, the straight line depreciation expense in the first accounting year and the last accounting year is usually lower.

For example, suppose an asset having a depreciable cost of $5000 and a useful life of 5 years is purchased in the middle of an accounting year. In that case, the amount of depreciation expense in the first accounting year will be half of the full year’s depreciation charge.

Plotting the depreciation expense of such asset over the accounting years that fall within its useful life would look something like this on a graph:

Don’t worry if you’re wondering how each year’s depreciation charge was calculated above.

The following sections will guide you through each step involved in calculating the straight line depreciation for each year of an asset’s life. Make sure to read the example below and solve the quiz towards the end!

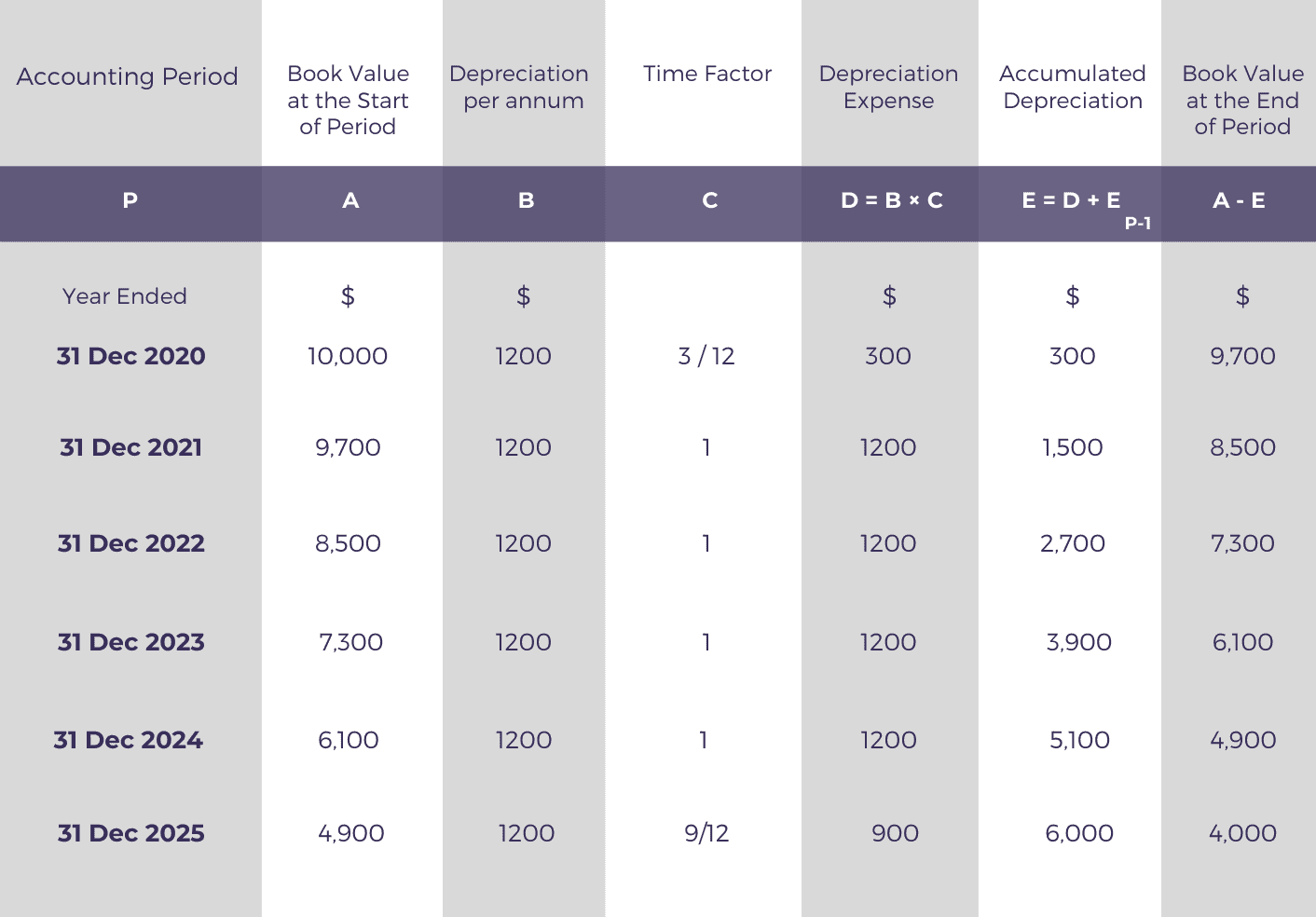

Bill bought a car for his business on 1 October 2020.

The car cost Bill $10,000 and has an estimated useful life of 5 years, at the end of which it will have a resale value of $4000.

Suppose Bill prepares his financial statements on 31 December.

What is the amount of depreciation expense and net book value to be recorded in each accounting year using the straight-line method?

The first thing we need to calculate is the annual depreciation charge using the straight line method formula:

[$10,000 (Cost) MINUS $4000 (Salvage Value)] Divided by 5 (Useful Life in Years) which works out to $1200 per annum.

Using this amount, we can calculate the depreciation expense, accumulated depreciation, and carrying value of the asset for each year as follows. In case you’re confused at any step, read the explanation below the depreciation schedule.

The depreciation expense is charged in full in all accounting years other than the first and the last accounting year.

In the first accounting year, the asset is available only for 3 months, so we need to restrict the depreciation charge to only 3/12 of the annual expense.

Similarly, in the last accounting year, we need to reduce the depreciation expense to just 9 months because the asset will complete its useful life at the end of the ninth month of the year 2025. Beyond this point, no further depreciation will be charged.