Accelerated depreciation techniques charge a higher amount of depreciation in the earlier years of an asset’s life. One way of accelerating the depreciation expense is the double decline depreciation method.

In this lesson, I explain what this method is, how you can calculate the rate of double-declining depreciation, and the easiest way to calculate the depreciation expense.

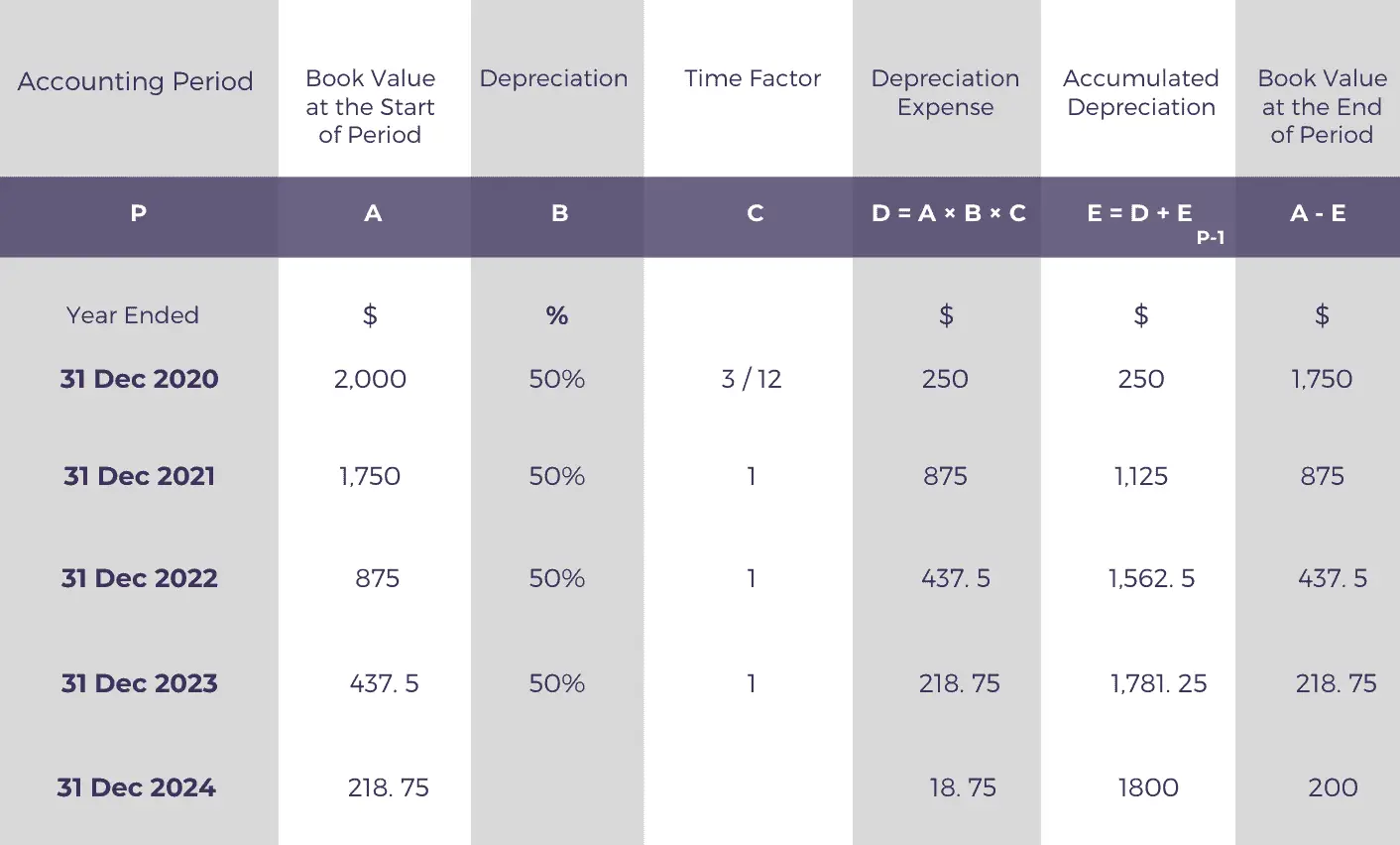

Here’s the depreciation schedule for calculating the double-declining depreciation expense and the asset’s net book value for each accounting period. In case of any confusion, you can refer to the step by step explanation of the process below.

To calculate the double-declining depreciation expense for Sara, we first need to figure out the depreciation rate.

Depreciation % = (2 × 100 ÷ 4)% = 50%

In the first year, we will only charge the depreciation expense for the three months that the laptop was available for use (from 1 October 2020 to 31 December 2020).

To calculate the depreciation expense for the first year, we need to apply the rate of depreciation (50%) to the cost of the asset ($2000) and multiply the answer with the time factor (3/12).

To calculate the depreciation expense of subsequent periods, we need to apply the depreciation rate to the laptop’s carrying value at the start of each accounting period of its life.

For example, the depreciation expense for the second accounting year will be calculated by multiplying the depreciation rate (50%) by the carrying value of $1750 at the start of the year, times the time factor of 1.

The time factor for any accounting period that falls between the first and the last period is 1 because the asset will be available for the entire period and, therefore, should be charged the depreciation expense in full.

The amount of final year depreciation will equal the difference between the book value of the laptop at the start of the accounting period ($218.75) and the asset’s salvage value ($200).

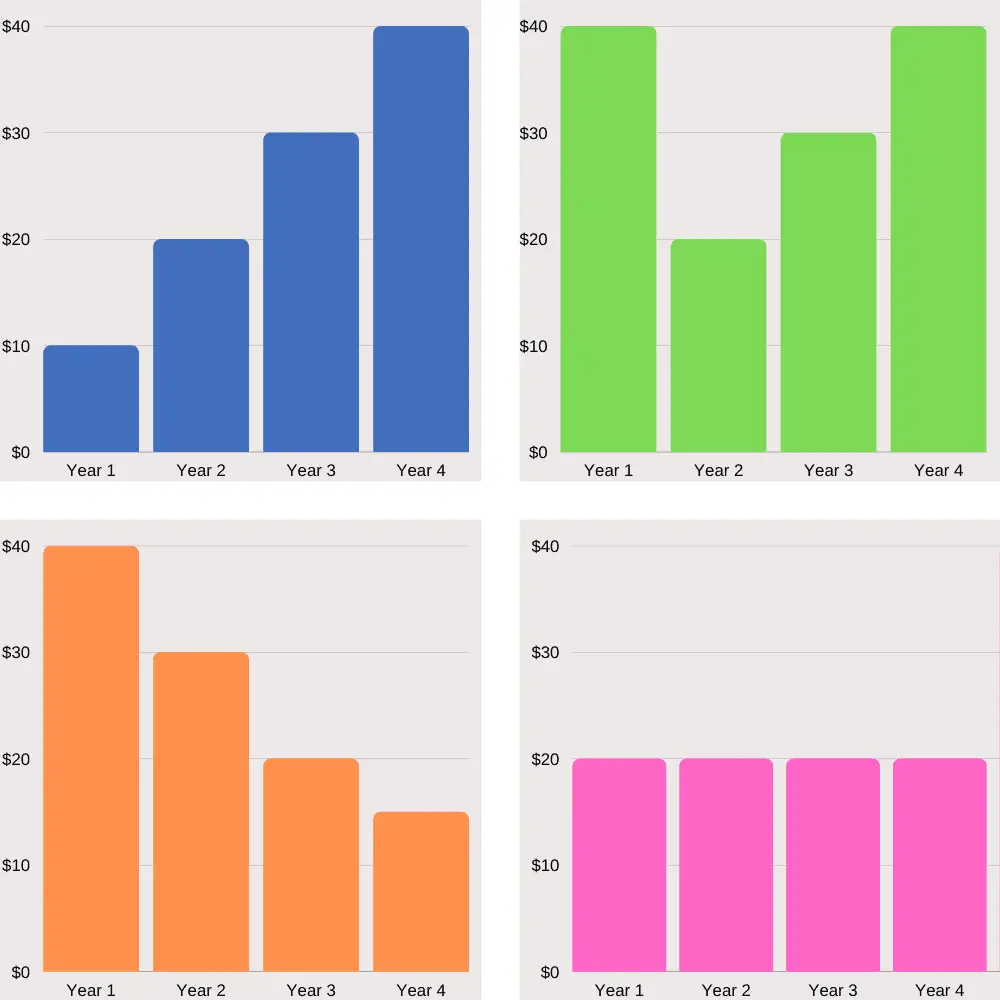

Which of the following graphs best illustrates the pattern of depreciation expense charged under the double-declining method over an asset’s useful life?