A delivery truck is acquired on 1 January 2020 for $12,000 and has:

- A useful life of 4 years

- A salvage value of $2000

Using the sum of the years’ digits method, What is the amount of depreciation expense of the delivery truck to be recorded in the financial statements prepared on 31 December each year over its useful life?

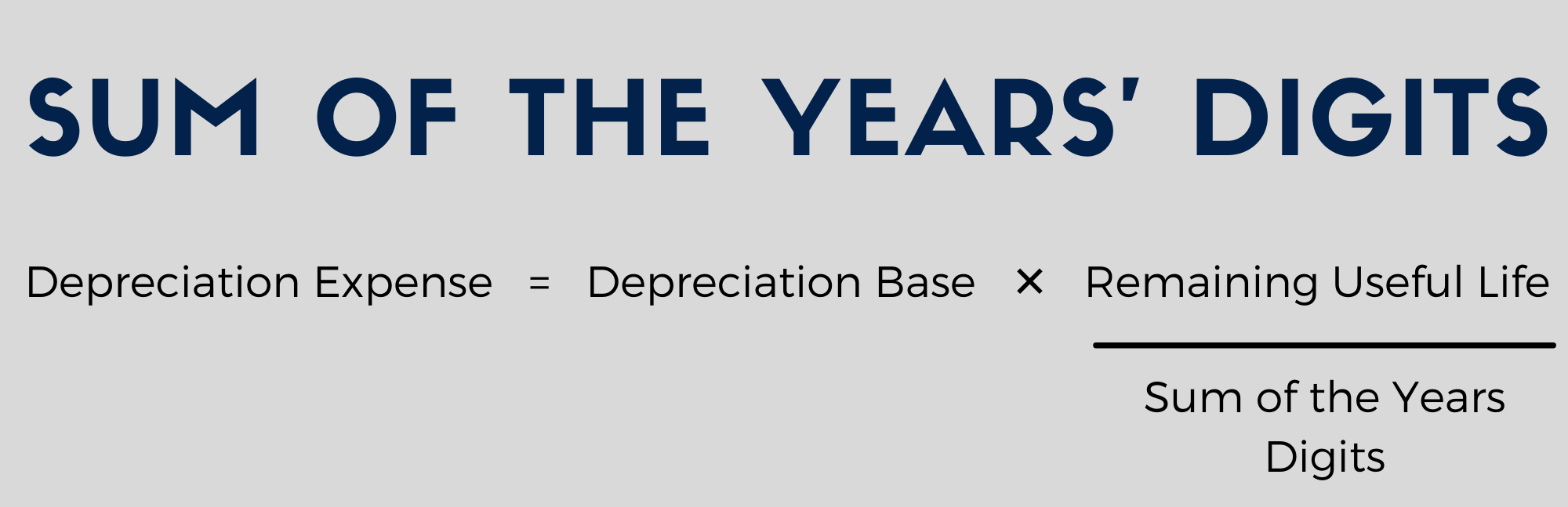

Step 1: Calculate Sum of the Years’ Digits

To figure out the depreciation expense of each year, we first need to calculate is the sum of the years digits. Since the useful life of the truck is four years, we need add all numbers that fall between 4 and zero to find the sum.

Sum of the years’ digits = 4 + 3 + 2 + 1 = 10.

Step 2: Calculate the Depreciation Base

We need to deduct the salvage value ($2000) from the initial cost ($12000) to calculate the delivery truck’s depreciation base.

Depreciation base = $12,000 – $2,000 = $10,000.

Step 3: Calculate the Remaining Useful Life

To find the delivery truck’s remaining useful life, we need to count it from the start of each year rather than the end. This may seem strange to you at first, but you will get the hang of it soon with practice.

For calculating depreciation for the first accounting period that ends on 31 December 2020 (Year 1), the remaining useful life of the delivery truck will be taken as 4 years. For the next accounting period that ends on 31 December 2021 (Year 2), the remaining useful life will be 3 years. For the Years 3 and 4, the remaining useful life will be 2 and 1 respectively.

Step 4: Calculate the depreciation expense

A delivery truck is acquired on 1 October 2020 for $12,000 and has:

- A useful life of 4 years

- A salvage value of $2000

Using the sum of the years’ digits method, What is the amount of depreciation expense of the delivery truck to be recorded in the financial statements prepared on 31 December each year over its useful life?

Step 1: Calculate Sum of the Years’ Digits

Sum of the years’ digits = 4 + 3 + 2 + 1 = 10.

Step 2: Calculate the Depreciation Base

Depreciation base = $12,000 – $2,000 = $10,000.

Step 3: Calculate the Remaining Useful Life

We need to count the remaining useful life from the asset’s timeline rather than the accounting periods’ perspective.

For calculating depreciation for the asset’s first year that ends on 30 September 2021 (Year 1), we will count the remaining useful life of 4 years. For the next year of the asset’s life that ends on 30 September 2022 (Year 2), the remaining useful life will be counted as 3 years. For Years 3 and 4 of the asset, the remaining useful life will be counted as 2 and 1, respectively.

Step 4: Calculate the depreciation expense

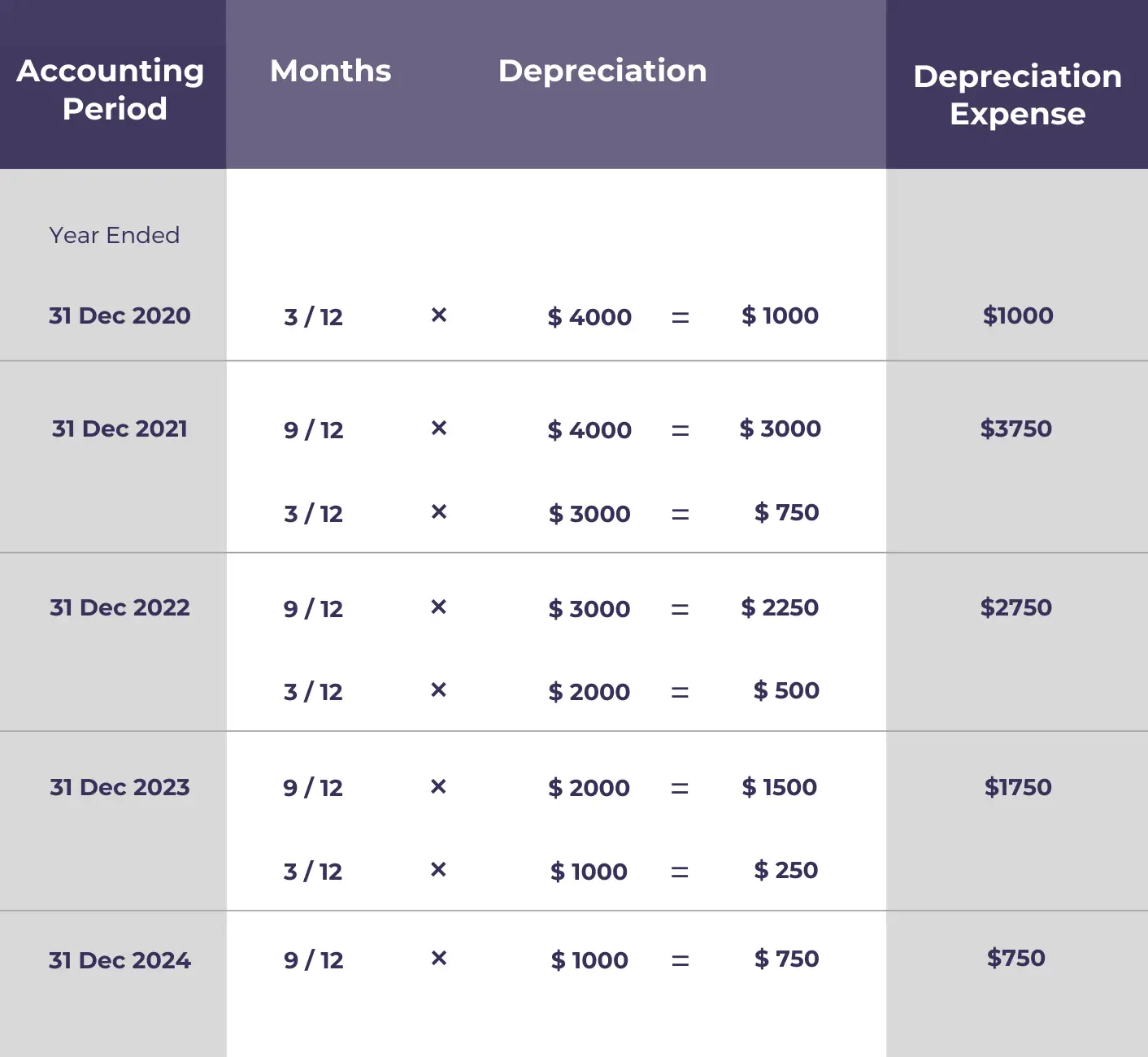

Before calculating how much depreciation is charged to each accounting period in Step 5, we first need to calculate the depreciation expense for each year of the asset life.

Step 5: Apportion the depreciation expense to the accounting periods

To calculate how much depreciation needs to be charged to each accounting period, we need to see the depreciation expense of each year of the asset (Step 4) that overlaps each accounting period.

For example, in the first accounting period that ends on 31 December 2020, only 3 months out of the first year of the asset overlaps. So we charge 3/12 of the first year’s depreciation expense ($4000) to the accounting period that ends on 31 December 2020.

In the second accounting period ending on 31 December 2021, 9 months out of the first year of the asset overlaps as well as 3 months out of the asset’s second year. Therefore, the depreciation expense for the second accounting period is equal to 9/12 ✕ $4000 plus 3/12 ✕ $3000.

Here’s the complete calculation for Step 5.

Question 5

Beth purchased a display shelf for her bakery costing $10,000 on 1 January 2020. The has a useful life of 4 years after which it is expected to have no residual value.

What is the net book value of the shelf that will appear on the balance sheet on 31 December 2021 if it is depreciated using the sum of the years’ digits method?