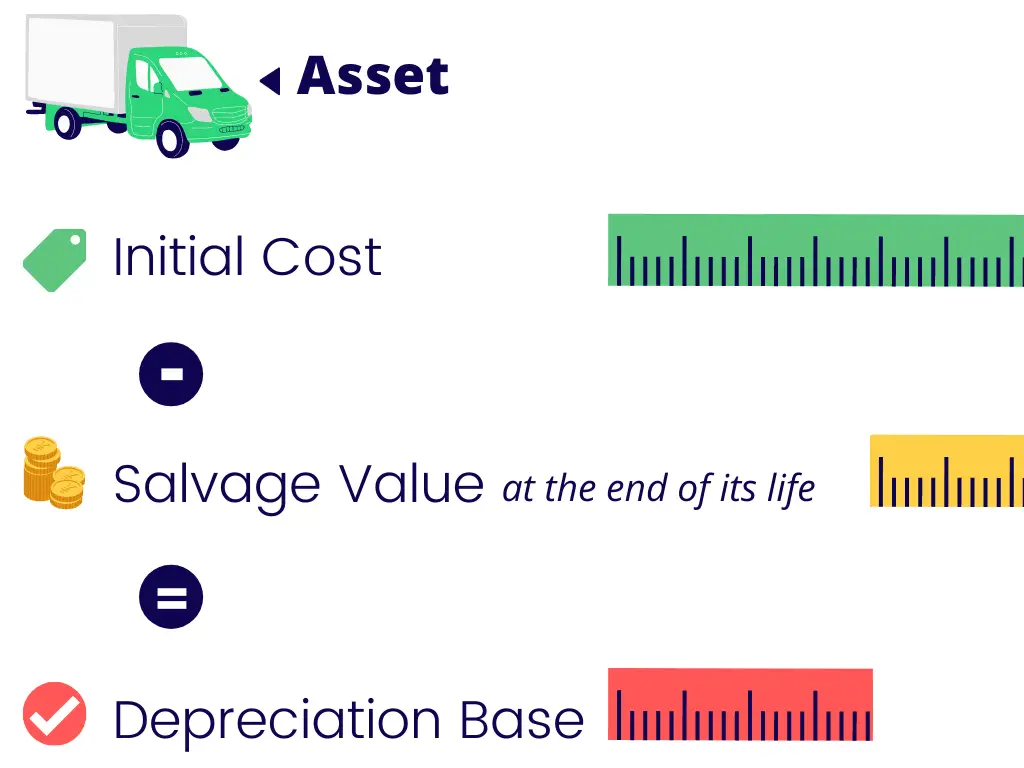

An asset’s depreciation base is the value that will be charged over its useful life as a depreciation expense using a suitable method such as the straight-line method or sum of the years’ digits method.

We need to calculate the depreciation base of assets because we do not want to depreciate the part of the asset’s cost that can be ‘salvaged’ at the end of its useful life.

To find the depreciation base, we need to add all capital expenditures that make up an asset’s initial cost and subtract any salvage value.

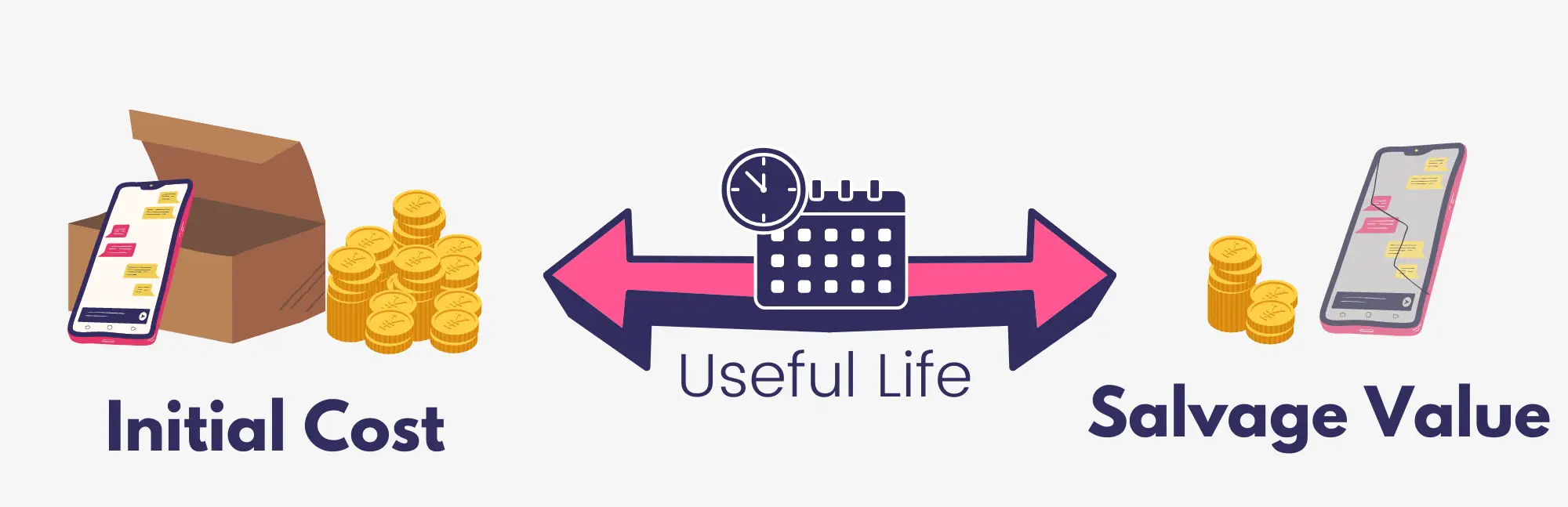

The original value of an asset is reduced each year by the amount of depreciation until it is finally reduced to its salvage or residual value at the end of its useful life.

Salvage value, also known as residual value or scrap value, is the estimated amount that an asset will fetch when it is disposed of at the end of its useful life.

You can determine the salvage value of an asset by taking into account:

- It’s useful life. The longer the asset is expected to be used, the lower its residual value;

- The current market value of similar assets that are more aged;

- Does the asset have an active market for resale? If it is a specialized asset, it might not fetch a good price towards the end of its life;

- Will any costs be incurred on disposal or removal of the asset? You may deduct these from the estimated revenue from the sale.

Barry ordered a printer costing $100 from a website for office use.

Barry also paid extra shipping costs of $10 to deliver the printer to the required business address.

In addition to the printer, Barry also bought a set of printer sheets from a stationery shop for $5.

The printer is expected to last for 5 years, after which Barry will scrap it for $20.

What is the printer’s depreciation base?