When you’re just starting to learn accountancy, it can be easy to confuse the expenses of a business with its assets. The distinction between these elements of financial statements is important for the accurate calculation of the profitability and worth of a business.

In this post, I will explain how to differentiate between assets and expenses and how you should treat both elements in the financial statements.

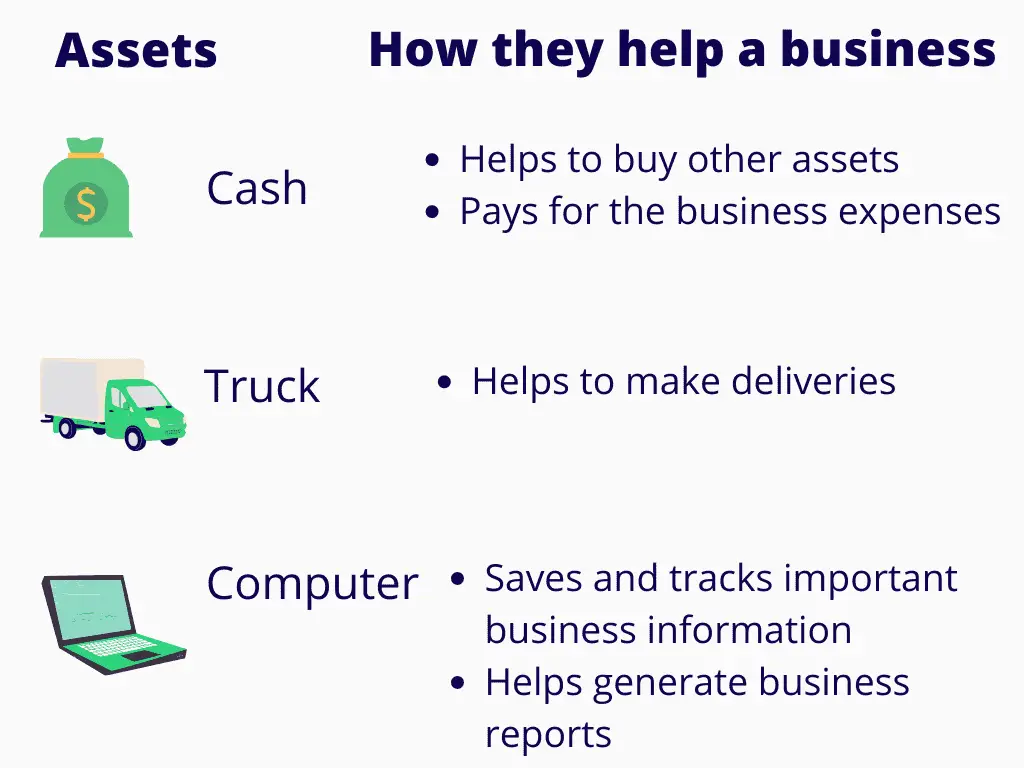

Assets include properties of all kinds that provide some value to a business in the future.

For example, cash is an asset that enables a business to pay for things in the future. A delivery truck is an asset that helps to transport things for a business.

On the other hand, expenses are the cost of resources consumed in the operations of a business during an accounting period. For example, the cost of serving meals is an expense of a restaurant.

Unlike assets, expenses do not provide a definite value to a business beyond the accounting period in which they are incurred.

For example, the manufacturing expense of a product that has already been sold to a customer has no obvious future value to a business. However, any inventory stocked in the warehouse is an asset of the business because it can be sold in the future to generate sales revenue.

The following infographic highlights the key differences between assets and expenses.

Following are examples of situations when the assets of a business are treated as an expense:

- It is uncertain if the business will acquire any economic benefits from the asset in the future.

For example, the cost incurred on researching a new production method cannot be capitalized as an asset because of the uncertainty regarding its commercial success.

For example, the cost incurred on researching a new production method cannot be capitalized as an asset because of the uncertainty regarding its commercial success.

- The asset is immaterial and, therefore, not relevant to the users of the financial statements. In such circumstances, the cost of tracking an asset over its useful life may exceed any benefit from the information.

For example, a tape dispenser costing $4 fits the definition of an asset. However, it makes sense to charge it as a stationery expense instead of treating it as a fixed asset and charging depreciation over its useful life.

For example, a tape dispenser costing $4 fits the definition of an asset. However, it makes sense to charge it as a stationery expense instead of treating it as a fixed asset and charging depreciation over its useful life.

Expenses are incurred either when there is a consumption of economic resources or when a business receives economic benefits.

- The cost of sales is expensed in the accounting period in which the sales revenue is earned.

- Administrative costs are recognized as an expense in the accounting period in which the related services or goods are acquired.

For example, an office assistant’s salary will be recorded in the accounting period in which he or she has rendered services for the business.

For example, an office assistant’s salary will be recorded in the accounting period in which he or she has rendered services for the business.

- Depreciation of a fixed asset is expensed in the accounting periods that fall within its useful life.

How much do you know about

Assets and Expenses?

Take the free below quiz and find out!