Assets are valuable resources that belong to a business, including:

- Physical properties such as buildings;

- Monetary items like cash; and

- Intangible things such as websites and trademarks.

Here are some more examples of the different types of assets.

Future economic benefits can mean different things for different assets.

Some assets provide direct economic benefits (e.g., inventory), whereas others indirectly contribute to the future cash flows of a business (e.g., office computer).

Here are some examples of assets and their future economic benefits.

- Cash is valuable to a business because it can pay for things in the future, such as salaries of employees, purchases from suppliers, and other assets.

- A machine can help a business to manufacture something that can sell for cash in the future.

- A warehouse can help a business store and retrieve inventory in the future.

- Inventory and receivables can turn into money in the future.

- Advance salary (prepaid expenses) entitles the business to receive the employee’s services in the future against that advance.

A business should be able to obtain benefits from an asset and restrict its access to others.

For example, ownership of a piece of land gives its owner the legal right to construct a building on it for its own use and prevent others from entering the property without permission.

Since accounting is based on historical transactions and events, any assets that appear on a balance sheet need to be previously acquired.

So far, I have explained what assets are, their characteristics, and types, but as an accounting beginner, it’s equally important for you to learn about what are not assets.

First on the list are resources that are unlikely to provide future economic benefits.

For example, if a customer who owed some money to the business files for bankruptcy, it should no longer be a valuable asset in its accounting books.

However, not all things that provide future economic benefits to a business are to be treated as an asset either in accounting. Here are some instances where this is the case.

If we cannot reliably measure an asset’s value, or the business does not control an asset, we cannot identify it as an asset in the accounting books.

For example, a restaurant cannot show its chef as an asset in its accounting books even if it is the most valuable resource of the business because:

- No one can place an objective value on the employee (i.e., lack of measurability).

- The restaurant cannot force its chef to work in the future (i.e., lack of control).

You cannot recognize a future asset now based on the expectation of a transaction or event that hasn’t already happened.

Like all accounting, assets are recognized when a past transaction establishes control over the asset.

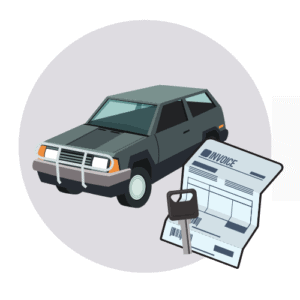

For example, suppose a car showroom places an order to purchase a vehicle from the car manufacturer on 1 December 2020. The showroom receives a brand new vehicle on 5 January 2021 and agrees to pay the car manufacturer’s entire sum in 3 months. In the meantime, the showroom is allowed to sell the new vehicle.

From an accounting perspective, the showroom cannot show the new vehicle in its accounting books until the day it has gotten control of the asset (i.e., on 5 January 2021). So if a balance sheet of the car showroom is prepared on 31 December 2020, it will not show the new car in the assets because the event that establishes its control over the asset has not occurred by then.

Lastly, a resource cannot be treated as assets when a business cannot restrict its benefit to others. Examples of such resources are clean air and public utilities.

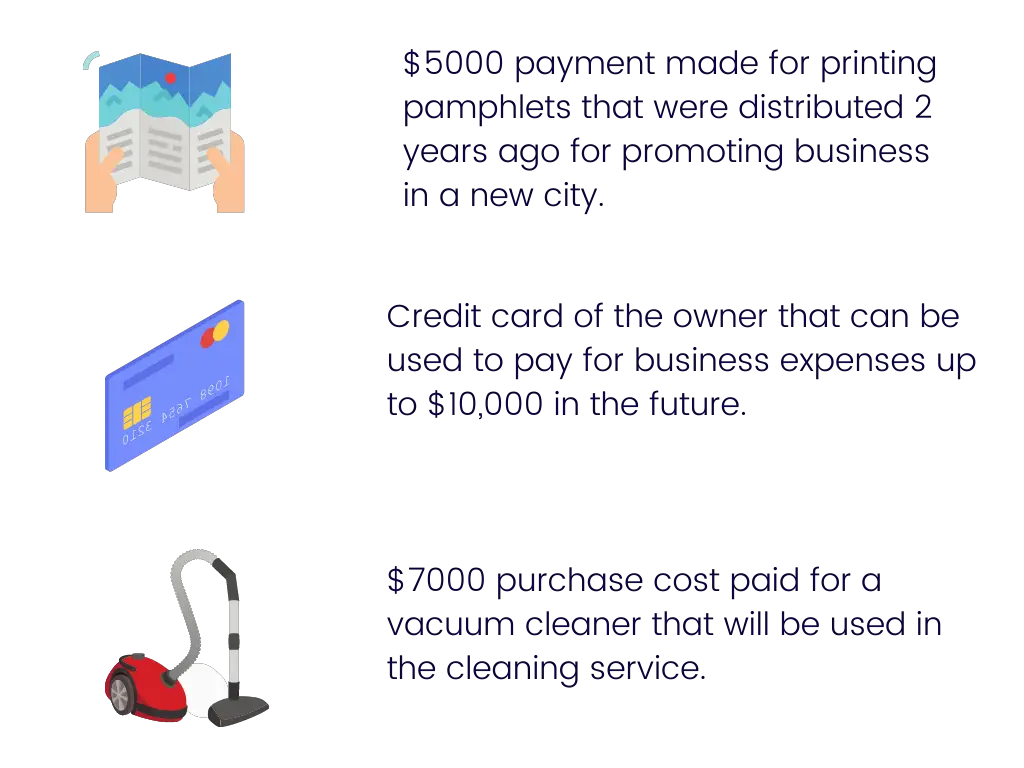

Which of the following is an asset for a carpet cleaning business?

Which of the following is a current asset?

Lou paid a 3-month advance amounting to $3000 for a small painting studio that she rented on 1 December 2020. The term of the rental agreement is 2 years but the owner can request Lou to vacate the property at anytime by serving a notice. The studio will cost Lou $1000 per month to rent and has a market value of $100,000.

What is the total value of assets that can appear in the balance sheet of Lou Studios on 31 December 2020 resulting from the above transaction?