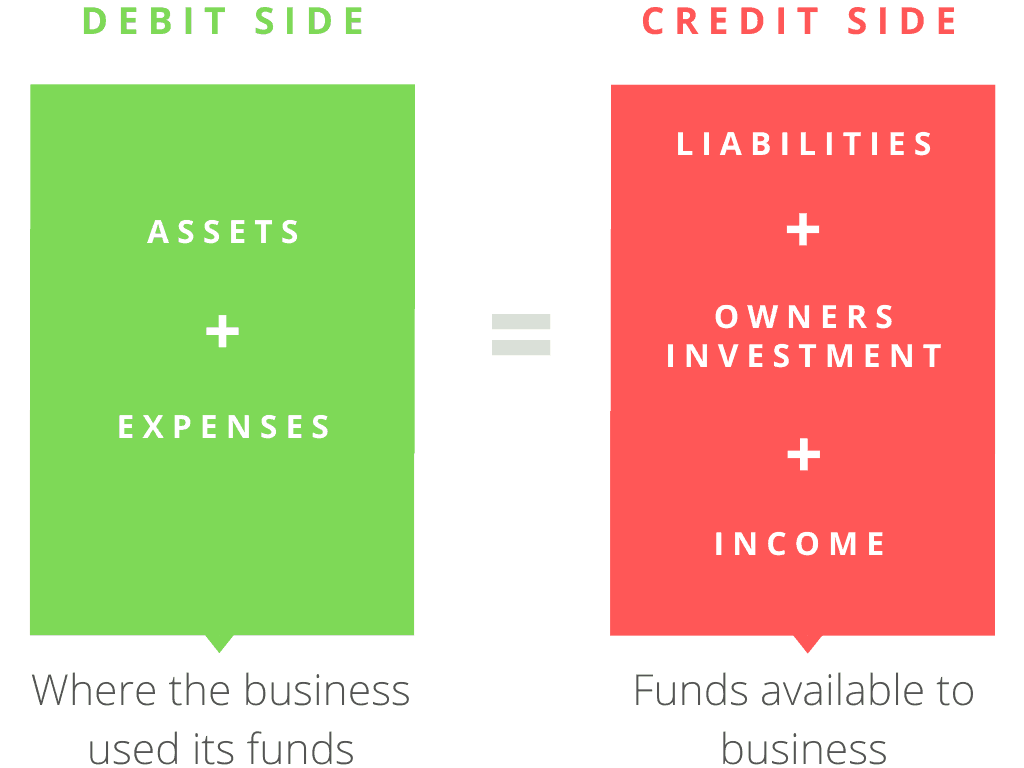

Funds of a business can be used to pay for expenses such as salaries, or they can be used to purchase assets such as equipment and inventory. Any unused funds are kept as cash in hand, or saved in a bank account (which are also assets).

If an accountant does not make any mistake in compiling the financial statements, it makes sense to say that the sum of assets and expenses of a business (debit side) should equal its available funds (credit side).

We can write this in the form of an accounting equation as:

Assets + Expenses = Liabilities + Owners Investment + Income

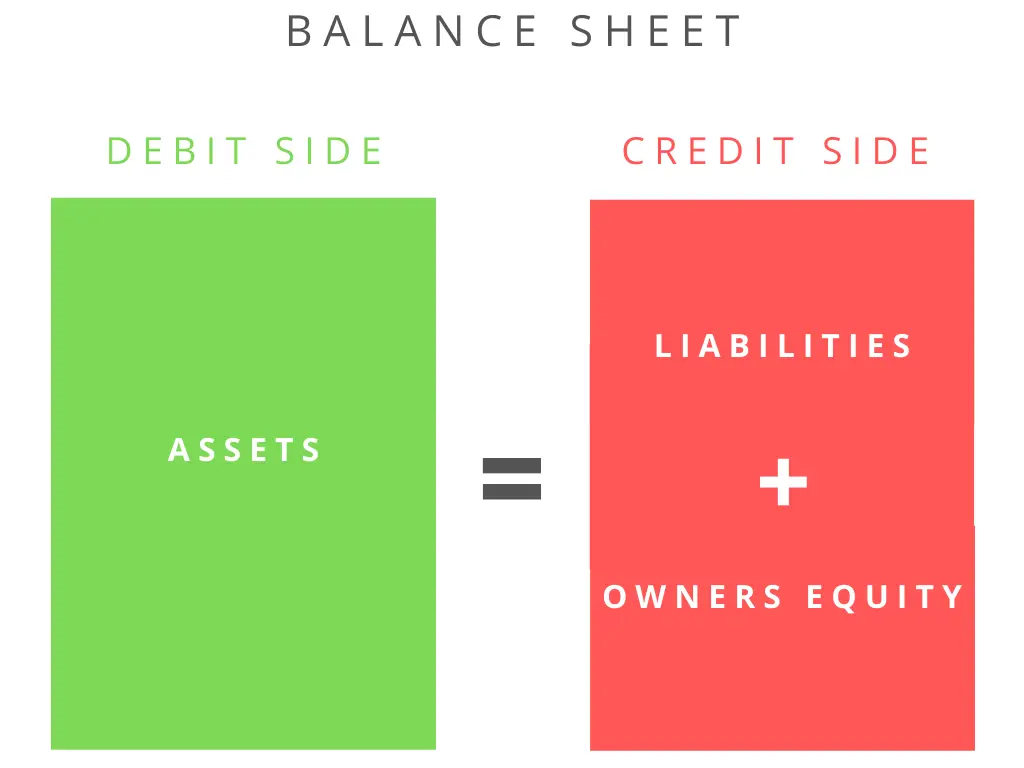

Note that the actual balance sheet is presented a bit differently from this equation, which we will discuss in the next section.

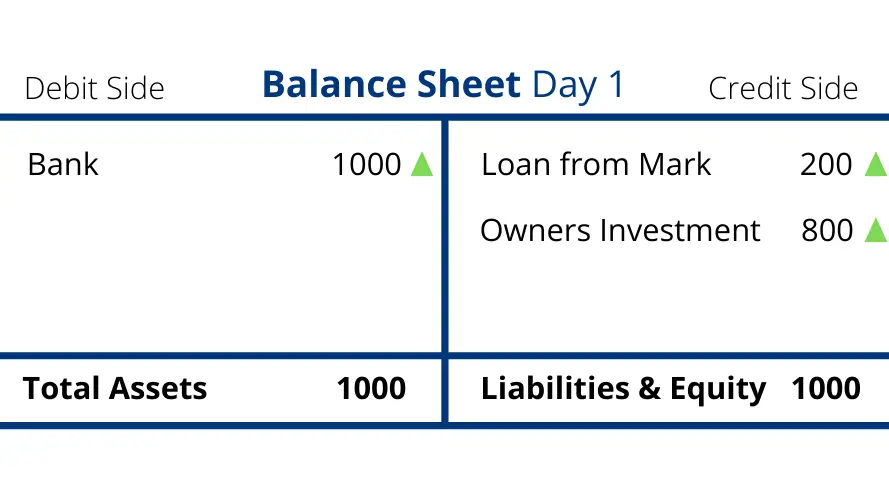

William decided to start a photography business as part of a week-long school project. He is required to prepare a balance sheet at the end of each day and make sure its totals always match.

Day 1

William opened a bank account for his business and deposited $1000 using his personal savings ($800) and a loan from his friend Mark ($200).

Both sides of the balance sheet match because the total funds that William raised for the business equal the total assets.

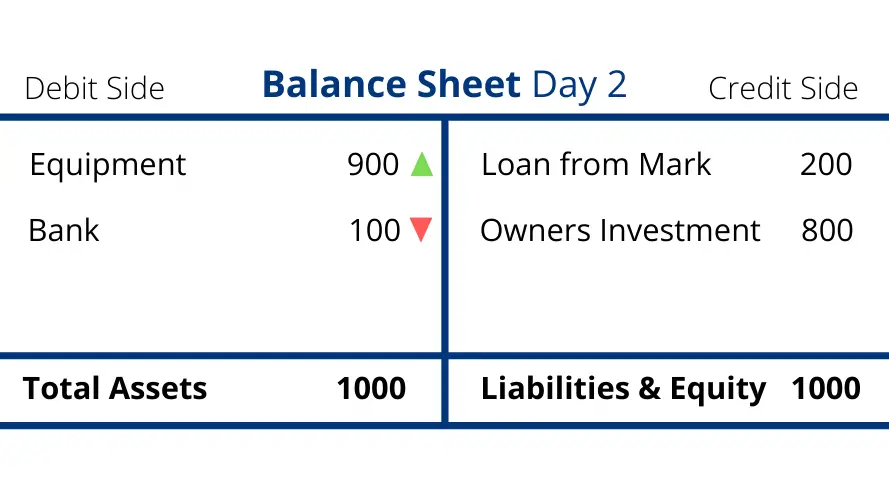

Day 2

William purchased photography equipment costing $900 paying from his bank account.

The balance sheet totals have not changed because the increase in one asset is canceled out by the decrease in another asset.

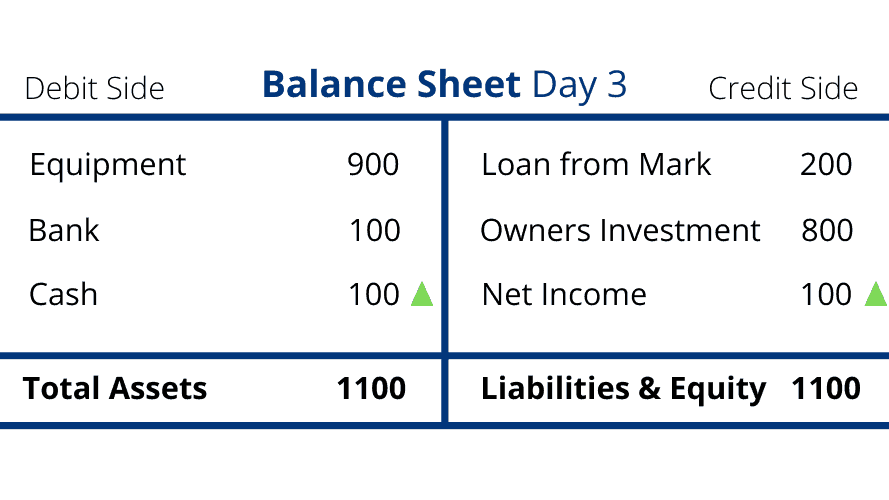

Day 3

William finally convinced someone to actually pay him for a photograph: his loving sister Jane.

He charged Jane $100 for a portrait which she paid in cash.

Income has increased both sides of the balance sheet by the same amount causing the balance sheet totals to agree once again.

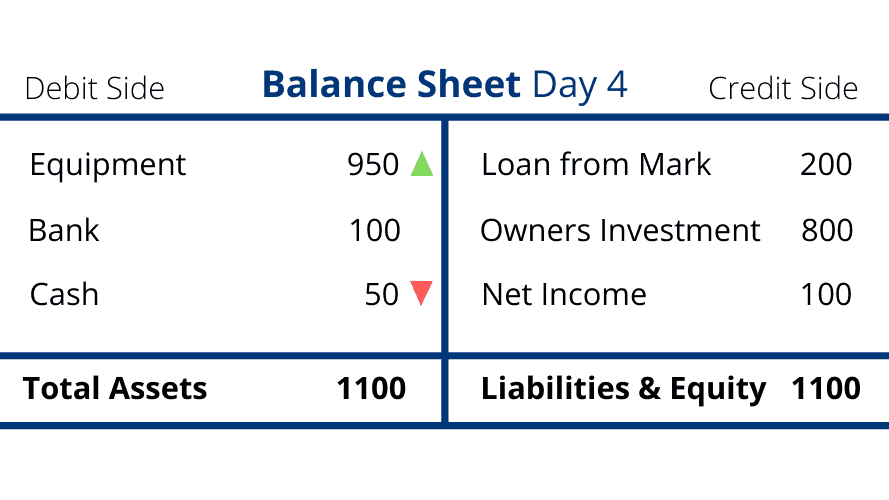

Day 4

William purchased a lens for his camera costing $50 in cash.

The transaction only changed the composition of the assets and not the total assets, which are once again equal to the total credits.

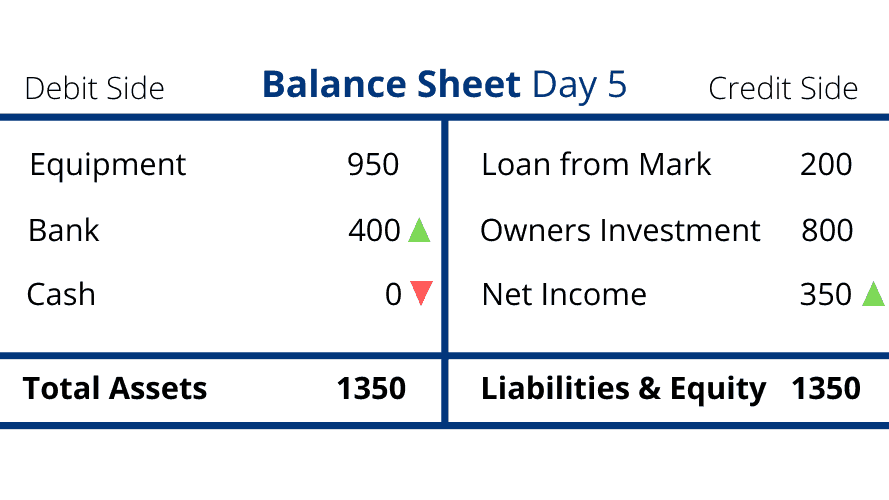

Day 5

William covered the engagement ceremony of his friend. He had to take a cab to reach the destination which cost him $50.

William charged a fee of $300, which was transferred to his bank account on the same day.

The credit side increased by $250, which is equal to the net increase in assets ($300 income less $50 expense).

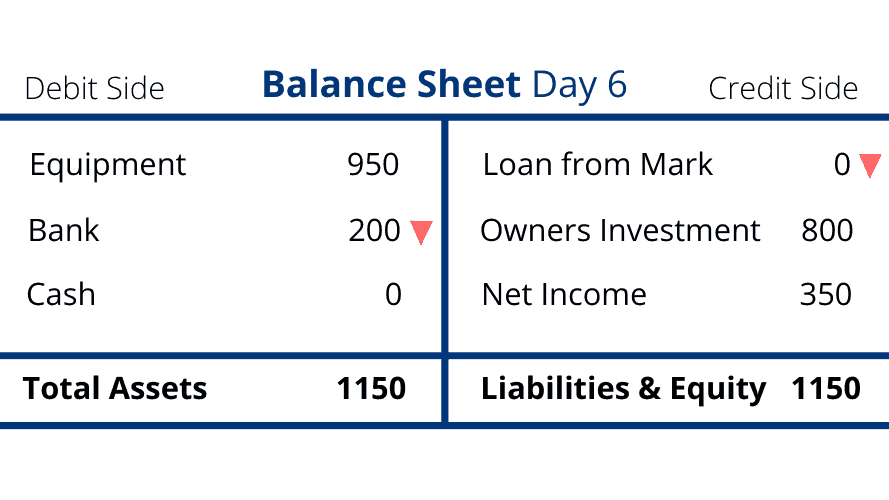

Day 6

William repaid his friend’s loan by transferring $200 from his bank account.

Assets and liabilities have decreased by the same amount.

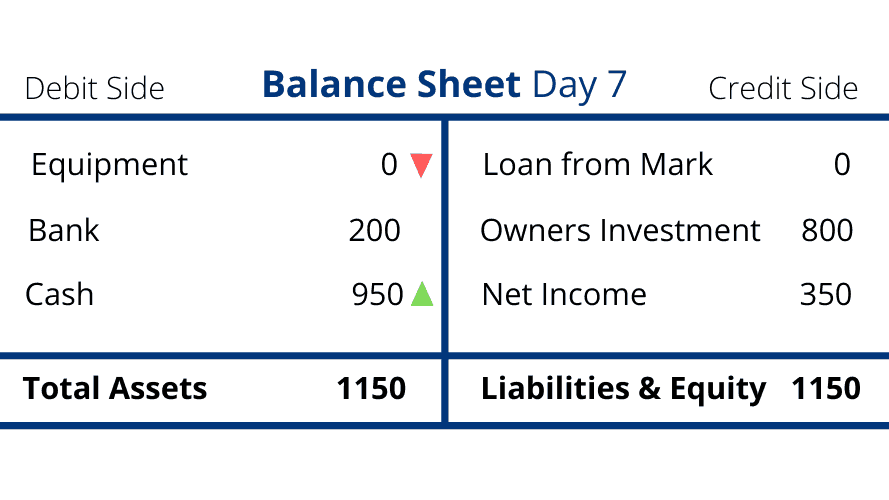

William returned all the equipment he had purchased to the store and requested a refund. The store has a one-month return policy so William received the full $950 in cash.

As expected, both sides of the balance sheet are equal at the end of the week.