Understanding how the accounting equation works is one of the most important accounting skills for beginners because everything we do in accounting is somehow connected to it.

In this lesson, I explain all you need to know about the accounting equation in the most simple way possible. Once you’ve mastered the accounting equation, do solve the quiz given at the end of the lesson to test your understanding!

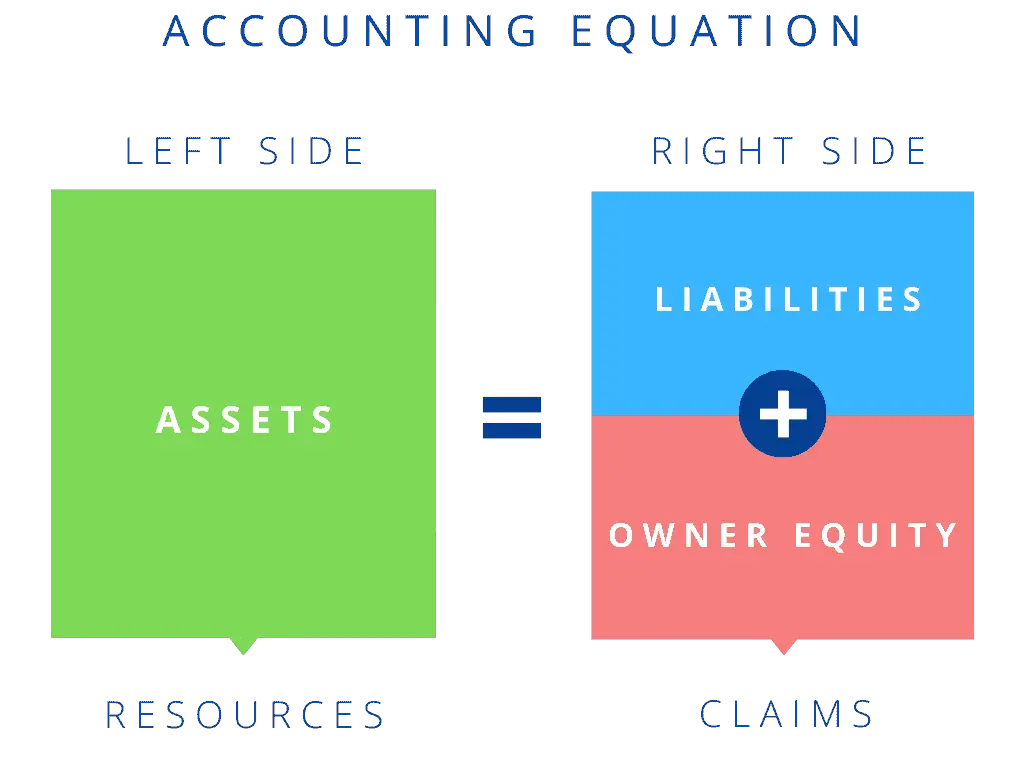

The accounting equation shows the amount of resources available to a business on the left side (Assets) and those who have a claim on those resources on the right side (Liabilities + Equity). Both sides of the accounting equation are always equal.

Before explaining what this means and why the accounting equation should always balance, let’s review the meaning of the terms assets, liabilities, and owners’ equity.

The accounting equation’s left side represents everything a business has (assets), and the right side shows what a business owes to creditors and owners (liabilities and equity).

The owner’s equity is the balancing amount in the accounting equation. So whatever the worth of assets and liabilities of a business are, the owners’ equity will always be the remaining amount (total assets MINUS total liabilities) that keeps the accounting equation in balance.

Mathematics aside, if we simply consider the fact that without any investment by owners (equity) and debt borrowed from creditors (liabilities), a business would have absolutely no resources. This implies that all assets that exist in the business must have been acquired from either:

- Loans from creditors (liabilities);

- Capital contributions by the owners (which is part of owner’s equity); or

- Internal funds that were retained from business profits (which is also part of owner’s equity).

Laura wants to turn her passion for yoga into her career by starting a yoga coaching business.

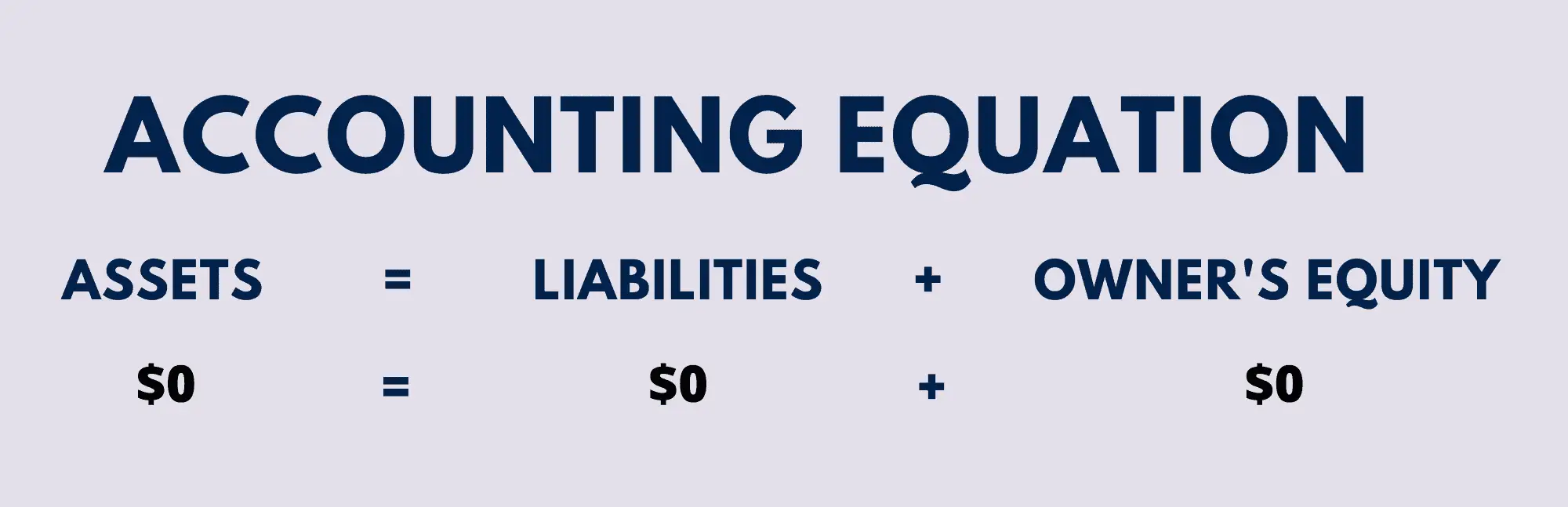

Like any brand new business, it has no assets, liabilities, or equity at the start, which means that its accounting equation will have zero on both sides.

In this example, we will see how this accounting equation will transform once we consider the effects of transactions from the first month of Laura’s business.

The following transactions took place on the first day of business:

- Laura deposited $5,000 from her personal bank account to a newly opened business account.

- Laura paid $200 to a consultant to help her with the business plan.

- Laura hired Chris on a monthly salary of $2000 to assist her in running the business. Chris received his first salary at the end of the first month.

- Laura got a permit from the city council to allow her to host her yoga classes in the park. The permit costs $1200 per annum.

- Laura’s friend Jim, a web developer, built a website for her business for $3600. Laura promised to pay Jim in full by the next month for his services. The website has a useful life of 24 months.

Following transactions happened during the rest of the month:

- Sixteen people got their first yoga lesson from Laura. Laura charges $200 per person and collects the fee at the end of each month. All besides Sara out of the sixteen paid their first-month fee by the end of the month. Sara cleared her dues in the following month.

Calculate the accounting equation of Laura’s business at the end of the first month.

To calculate the accounting equation, we first need to work out the amounts of each asset, liability, and equity in Laura’s business.

Here’s an explanation of how the values listed above have been calculated.

- To calculate the amount of cash at bank at the end of the first month, we start with the initial deposit by Laura ($5000) and subtract payments for the business consultancy ($200), Chris’s salary ($2000), and permit fee ($1200). The revenue collected from the fifteen clients who paid by the month-end is added to the total ($200 x 15).

- Website is an intangible asset of the business. Its cost ($3600) must be spread over its useful life (24 months which means that its value will decrease each month by $150 ($3600 / 24) and charged as an expense. Therefore, its value at the end of the first month works out to $3450 ($3600 – $150).

- You can think of the permit as a prepaid asset for Laura. Initially, it is recorded at its full cost ($1200), but as the permitted time (12 months) gets used up, $100 ($1200 / 12) must be subtracted from its total value each month and charged as an expense. Its value at the end of the first month will be $1100 ($1200 – $100).

- Although Laura didn’t get any payment from Sara at the end of the first month, the amount owed to the business ($200) should be recorded as a receivable asset in the accounting books.

- The business owes Jim $3600 for his web development services, so it must be shown in the accounting books as a liability.

- Laura’s seed capital into the business ($5000) is part of the owner’s equity.

- Retained profit includes the total income earned from 16 clients ($3200 [$200 x 16]) after subtracting expenses relating to consultancy ($200), salary to Chris ($2000), website amortization ($150), and permit fee for one month ($100).

This is how the accounting equation of Laura’s business looks like after incorporating the effects of all transactions at the end of month 1.

As expected, the sum of liabilities and equity is equal to $9350, matching the total value of assets. So, as long as you account for everything correctly, the accounting equation will always balance no matter how many transactions are involved.

Which of the following is the correct accounting equation?

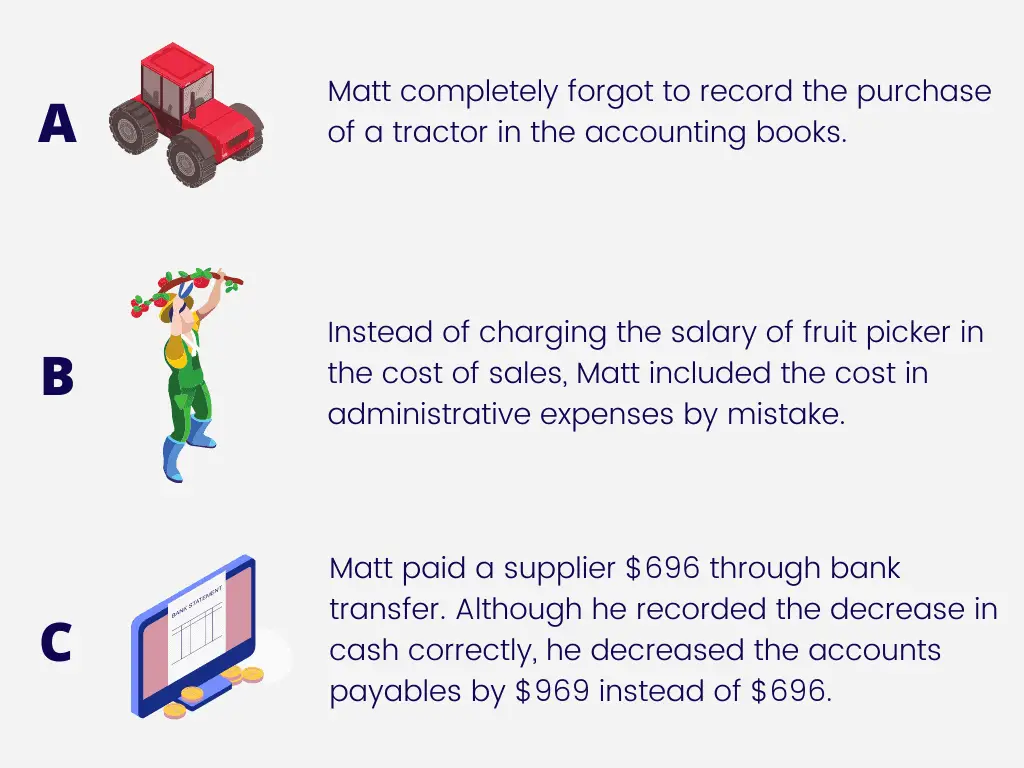

Matt cannot figure out why the accounting equation of his farming business is not balanced. Which of the following errors could explain the reason for the out-of-balance accounting equation for Matt?