Lynda sells a particular model of desktop computers on her website.

She launched her website in January this year, and charges a selling price of $900 per unit.

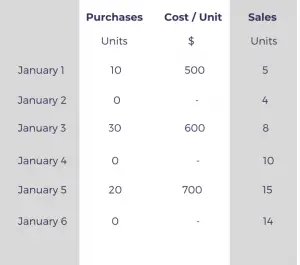

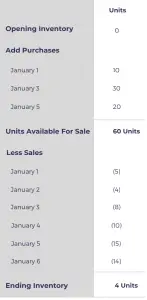

Details of her sales and purchases over the first six days of business are as follows:

Calculate the value of ending inventory, cost of sales, and gross profit for Lynda’s first six days of business based on the LIFO Method.

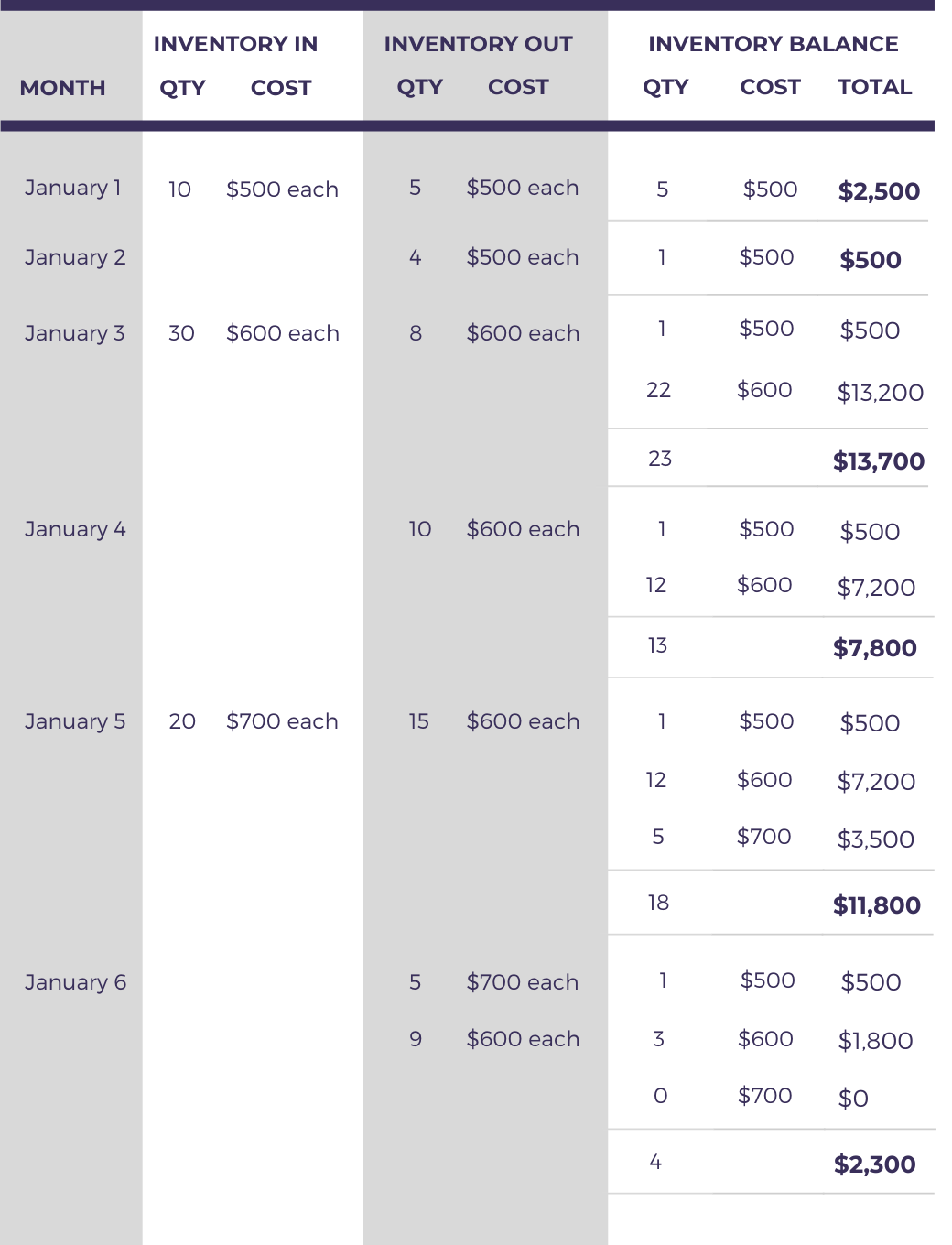

Ending Inventory

To find the value of ending inventory, we need to track additions and deletions in the computer units alongside its associated cost.

Based on the calculation above, Lynda’s ending inventory works out to be $2,300 at the end of the six days.

Let’s break down the process involved in arriving at the above value of ending inventory.

The first step is to note the additions in inventory in the left column, along with the purchase cost for each day. For example, on the first day, 10 units of inventory were added at the cost of $500 each, which we will record as follows.

Second, we need to record the quantity and cost of inventory that is sold using the LIFO basis.

If the inventory units sold during a day are equal or less than the inventory units purchased during the same day, we will assign that day’s cost to the inventory sold because it is the most recent purchase cost.

For example, only five units are sold on the first day, which is less than the ten units purchased that day. We will therefore assign $500 to each sale made that day.

Lastly, we need to record the closing balance of inventory in the last column of the inventory schedule.

To take the first day as an example, we can find the closing balance by deducting the number of units sold (5) from the number of units purchased (10), which is five units, and assign it the cost value of $500 each to calculate the total amount of $2500 (5 x $500).

When inventory balance consists of units with a different value, it is important to show those separately in the order of their purchase. Doing so will ensure that the earliest inventory appears on top, and the latest units acquired are shown at the bottom of the list.

For example, the inventory balance on January 3 shows one unit of $500 that was purchased first at the top, and the remaining 22 units costing $600 each that were later acquired shown separately below. The total number of units at the end of that day is 23.

The reason for organizing the inventory balance is to make it easier to locate which inventory was acquired most recently.

When the inventory units sold during a day are less than the units purchased on the same day, we will need to assign cost based on the previous day’s inventory balance.

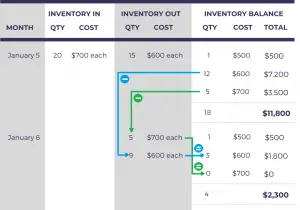

For example, on January 6, a total of 14 units were sold, but none were acquired. This means that all units that were sold that day came from the previous day’s inventory balance.

Out of the 18 units available at the end of the previous day (January 5), the most recent inventory batch is the five units for $700 each.

So out of the 14 units sold on January 6, we assign a value of $700 each to five units with the remainder of 9 units valued at the cost of the next most recent batch ($600 each).

Once the value of ending inventory is found, the calculation of cost of sales and gross profit is pretty straight forward.

Cost of sales

To calculate the cost of sales, we need to deduct the value of ending inventory calculated above from the total amount of purchases.

Gross Profit

Deducting the cost of sales from the sales revenue gives us the amount of gross profit.

Let’s calculate the value of ending inventory using the data from the first example using the periodic LIFO technique.

The first thing we need to calculate is the units of ending inventory.

Now that we know that the ending inventory after the six days is four units, we assign it the cost of the most earliest purchase which was made on January 1 for $500 per unit.

Value of ending inventory is therefore equal to $2000 (4 x $500) based on the periodic calculation of the LIFO Method.

This is slightly different from the amount calculated on the perpetual basis which worked out to be $2300.

The reason for the difference is that the periodic method does not take into account the precise timing of inventory movement which is accounted for in the perpetual calculation. Due to the simplification in the periodic calculation, slight variance between the two LIFO calculations can be expected.