Amy recently opened a grocery store. She wants to figure out her profitability for each product category at the end of her first week of operation.

On Day 1, Amy purchased 50 bottles of a particular soda brand at the cost of $10 per bottle.

On Day 3, Amy bought 100 more bottles at the cost of $10.2 per bottle.

On Day 6, Amy purchased an additional 15 bottles at the cost of $10.76 per unit.

Amy sold the 90 bottles in the first week for $14 apiece in the following order:

Day 1 10 units

Day 2 15 units

Day 3 20 units

Day 4 5 units

Day 5 15 units

Day 6 0 units

Day 7 25 units

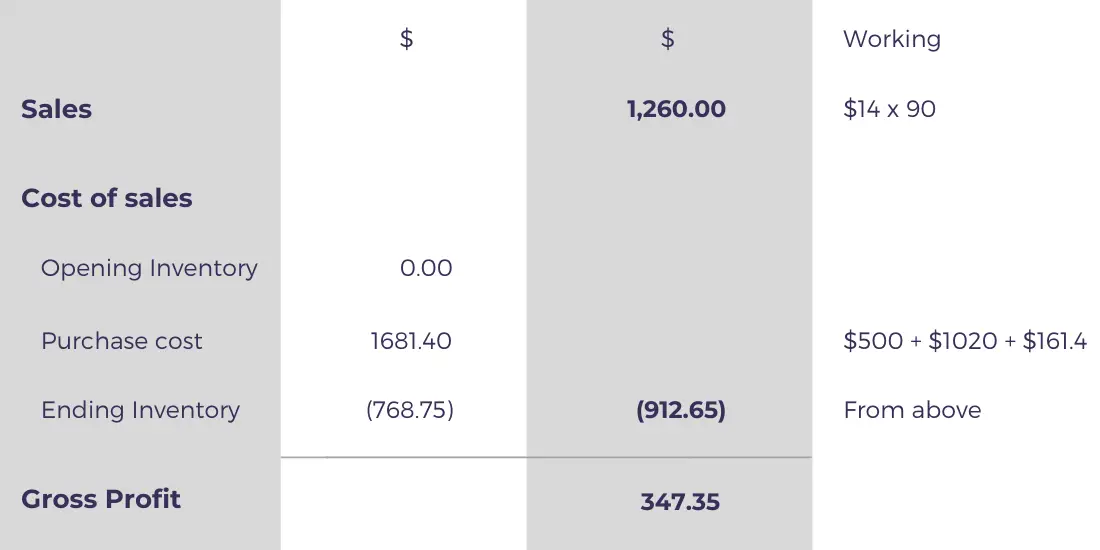

Using the Average Cost Method, calculate the values of ending inventory, cost of sales, and gross profit at the end of the first week.

The value of Amy’s ending inventory of the soda bottles is $768.75 (75 units valued at $10.25 each) at the end of Day 7.

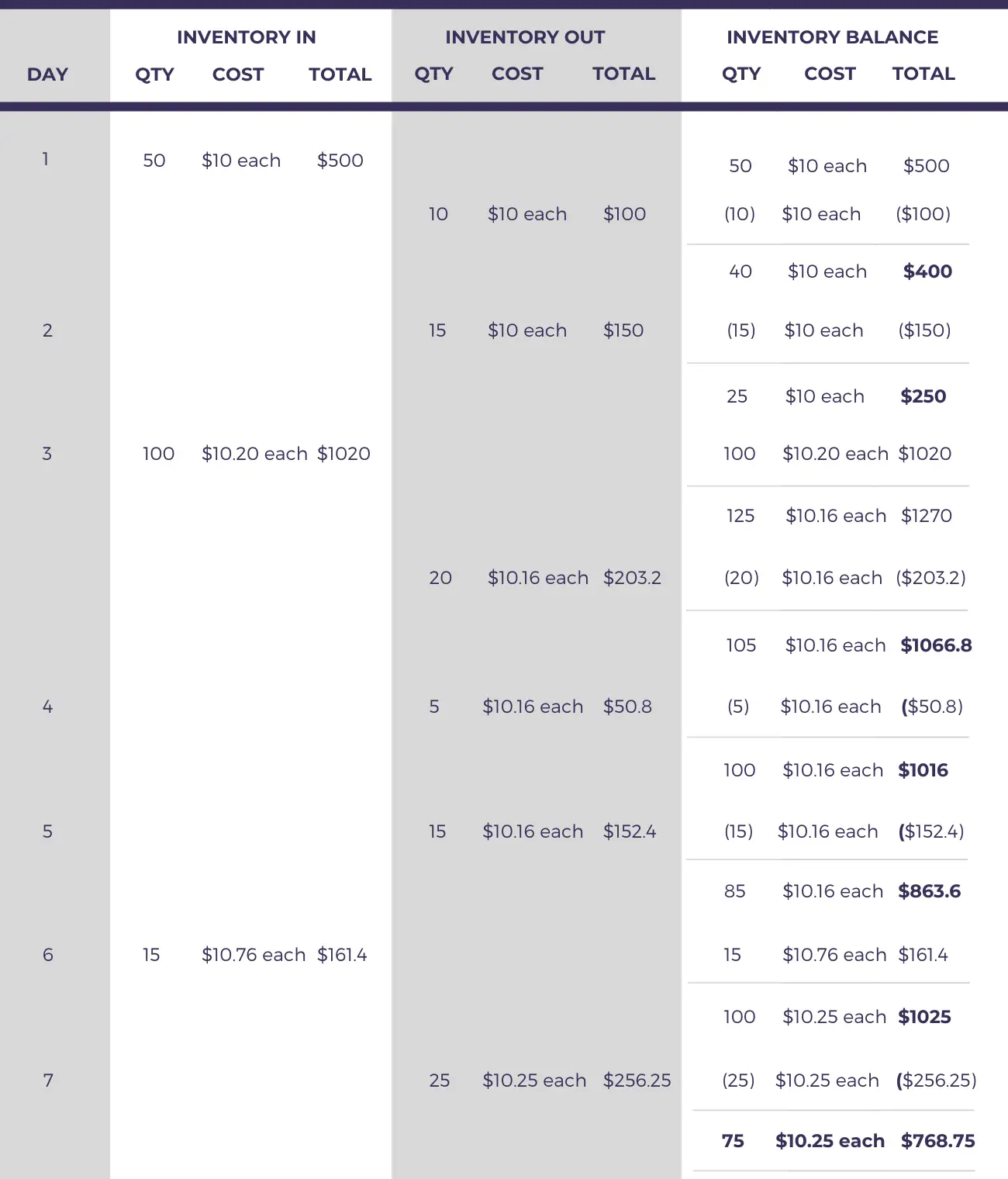

To arrive at this number, we have recalculated the average inventory cost after each addition and applied to each subsequent inventory issue until the next purchase.

For example, on the first day, the purchase cost is $10, which is charged as the cost of all sales made until the next purchase made on the third day (i.e., sales on Day 1 and Day 2).

To recalculate the average cost after each addition:

- We take the opening balance before the addition.

- Add the new units and their total cost in the opening balance.

- Divide the new total cost by the new total units in inventory.

For example, on day 3, we add the units and total cost of the new purchase (100 units and $1020) to the opening balance (25 units and $250). We then divide the new total cost of $1270 ($1020 + $250) by the new total units of 125 (100 + 25) to calculate the new average cost of $10.16 ($1270 ÷ 125).

We don’t need to recalculate the average cost until another batch of inventory is added to the mix, which would alter the cost.

If the inventory is purchased and sold on the same day, it is essential to first recalculate the average cost after accounting for the additions that day before valuing the units sold.

Once the value of ending inventory is found, the steps to calculate the cost of sales and the gross profit are quite simple.

You could also calculate the cost of sales by adding up the inventory issue costs in the second column of the ending inventory calculation, which would also give the same answer.

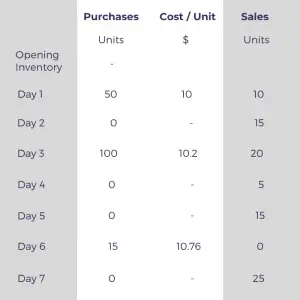

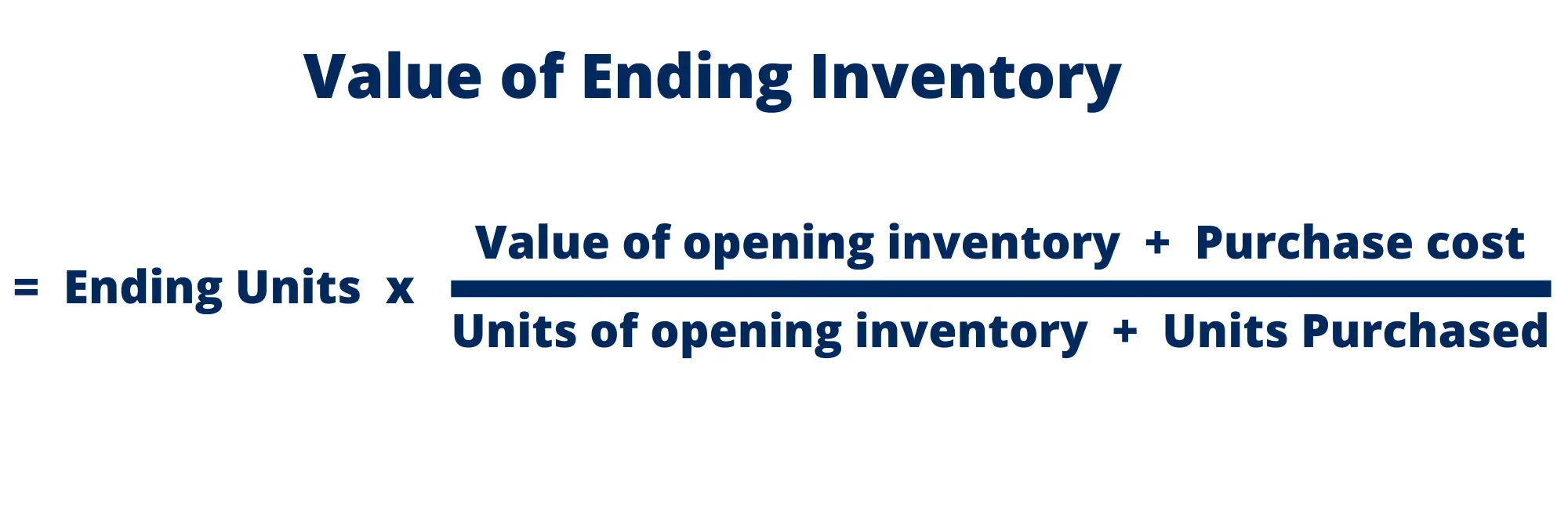

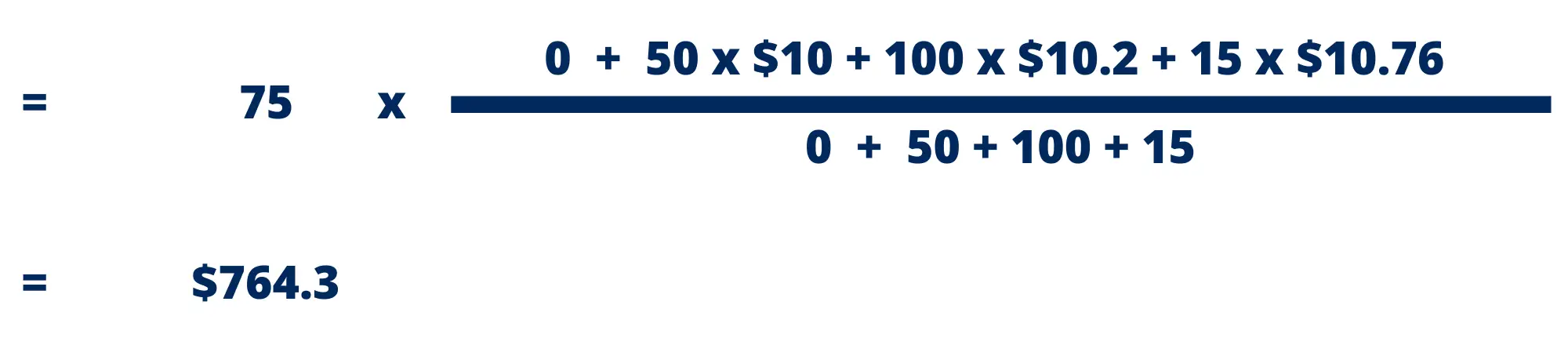

Using the first example, let’s calculate the value of ending inventory using the periodic average cost method.

To recap, we have the following data about Amy’s sales and purchases in the first week:

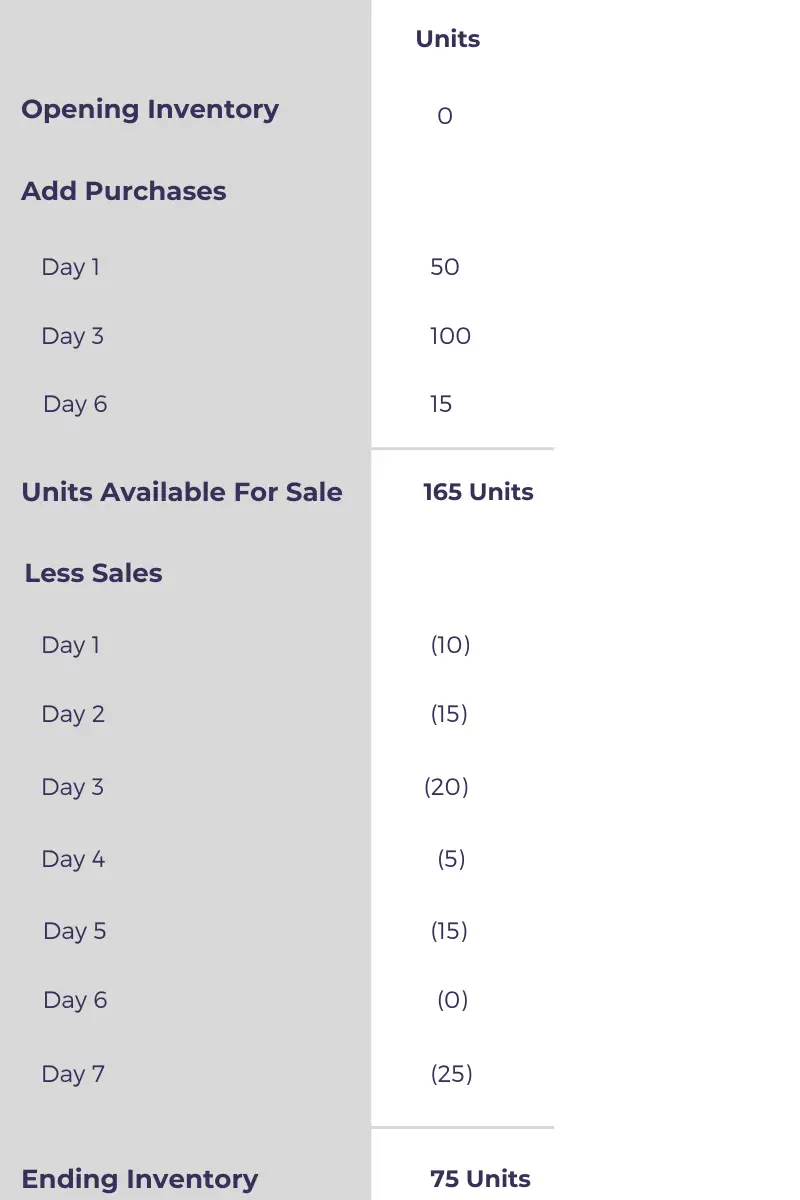

The first step in finding the ending inventory value is to calculate the units of ending inventory.

Ending inventory is the sum of opening inventory and the units purchased during the period minus inventory units sold, which is calculated as follows:

Now that we know there are 75 units of ending inventory, we can calculate the ending inventory value using the formula below.

Note that this value is slightly different from the one calculated using the perpetual average cost method.

On 1 January, a shop has 10 units of a specific type of gaming device in inventory valued at $25 per unit.

On 2 January, more units costing $40 per unit are added to the inventory.

The shop sold 5 units each on 1 January, 2 January, and 3 January.

a) What is the value of ending inventory on 3 January based on the perpetual average cost method?