Direct Material Price Variance (DMPV) shows the amount by which the total cost of raw materials has deviated from the planned cost as a result of a price change over a period.

In this post, I explain the two ways of calculating the DMPV using a simple example and how you can investigate possible causes of the variance by co-relating with other information. Be sure to check out the free quiz at the end of the post to test your understanding!

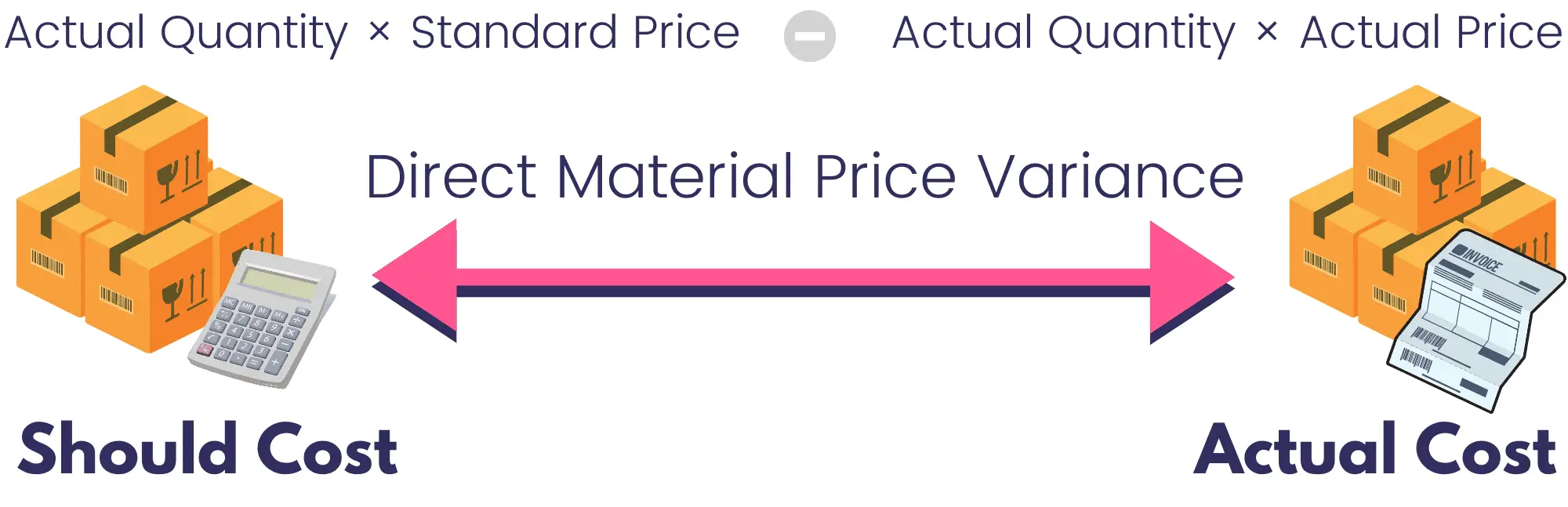

Direct Material Price Variance

Direct material price variance is the difference between what was actually spent on the raw materials purchased during a period and the standard cost that would apply if the materials were bought at the standard rate. To calculate the variance, we multiply the actual purchase volume by the standard and actual price difference.

Quick Note

The direct material price variance is also known as direct material rate variance and direct material spending variance.

How to Calculate Material Price Variance

The left side of the DMPV formula estimates what the actual quantity of direct materials purchased should cost according to the standard price allowed in the budget. The right side of the formula calculates what the direct materials actually cost during the period.

The difference between the standard cost (AQ × SP) and the actual cost (AQ × AP) gives us the material price variance amount.

We can simplify the DMPV formula by multiplying the actual purchase quantity by the price difference, as shown below.

Both formulas give the same answer so feel free to use whichever seems easier to you. Now let’s see these formulas in action in the example below.

Example

During the recent period, Teddy Bear Company purchased 20,000 bags of stuffing material for manufacturing stuff toys.

The standard price of $100 per bag was allowed in the budget, but the purchase manager was able to source the materials from a cheaper supplier at the cost of $80 per bag.

Calculate the direct material price variance (DMPV) for the period.

DMPV = Actual Quantity × Standard Price – Actual Quantity × Actual Price

DMPV = 20,000 × $100 – 20,000 × $80

DMPV = $2000,000 – $1600,000

DMPV = $400,000 Favorable

The material price variance in this example is favorable because the company was able to get the materials at a lower cost compared to the budget.

We can also calculate the price variance using the second formula.

DMPV = Actual Quantity × ( Standard Price – Actual Price )

DMPV = 20,000 × ( $100 – $80 )

DMPV = 20,000 × $20

DMPV = $400,000 Favorable

The following sections explain how management can assess potential causes for a favorable or adverse material price variance and devise a suitable response to the variation.

Favorable Direct Material Price Variance

If the actual price is lower than the standard price, we say that the direct material price variance is favorable because it cost the business lesser than expected.

Here are possible causes for a favorable direct material price variance:

- The lower price of materials is at the expense of lower quality. This is likely when there is an increase in customer returns, refund claims, quality control rejects, customer complaints, and an adverse material usage variance.

- The business has received bulk discounts from suppliers because of an increase in the average order size.

- The standard price was set too high in the budget.

- Market conditions have not allowed the actual prices to rise above the standard prices. This can be due to new suppliers entering the market, a decrease (or lower than expected increase) in import duties, etc.

- The purchasing staff has reached out to more suppliers for quotations, they have negotiated prices with suppliers better and have scouted more opportunities for bargains. Someone is getting a pay raise!

Adverse Direct Material Price Variance

If the actual purchase price is higher than the standard price, we say that the direct material price variance is adverse or unfavorable. This is because the purchase of raw materials during the period would have cost the business more than what was allowed in the budget.

Let’s take a look at some reasons that could explain an adverse direct material price variance:

- Better quality materials have been acquired at a higher price. This should be noticeable from drops in the number of returns by customers, refund claims, internal quality control rejects, and a favorable material usage variance.

- During the planning phase, the standard price was just set too low.

- Market conditions such as a supply shortage during the last period have unexpectedly driven up the cost of inputs.

- The purchasing staff hasn’t been pulling their full weight behind price negotiations, or they have been lazy in getting quotations from new suppliers to expand the supply pool. In this case, the management can actually play a role by hiring, firing, providing feedback, and retraining to the purchasing staff along with an overall review of the organization’s purchasing practices.

Question 1

DMPV = ________ Quantity × ( Standard Price – Actual Price )

Standard

Incorrect.

Actual

You're right!

Material price variance uses the actual purchase volume rather than the standard quantity.

Question 2

The direct material price variance is favorable if the actual price of materials is __________ than the standard price.

Lower

That is correct!

Higher

Incorrect.

Question 3

The standard price of raw materials is $4 per unit and the actual purchase quantity is 500 units. If the direct material price variance is $1000 adverse, what is the actual selling price of the raw material?

$6

Spot on!

The trick was to substitute the knowns into the variable formula:

DMPV = AQ × (SP - AP)

-1000 = 500 × (4 - AP)

-1000 / 500 = 4 - AP

-2 = 4 - AP

-2 -4 = - AP

-6 = - AP

AP = $6

$5

Incorrect.

$4

Wrong answer. The actual price must exceed the standard price because the material price variance is adverse.

$3

Not correct.

$2

Incorrect.

Question 4

Standard Quantity: 10,000 units

Actual Quantity: 9,000 units

Standard Price: $3 per unit

Actual Price: $4 per unit

What is the direct material price variance?

$10,000

Favorable

Wrong answer.

$9,000

Favorable

Not correct.

$10,000

Adverse

Incorrect.

$9,000

Adverse

You're right!

DMPV = AQ × (SP - AP)

DMPV = 9000 × (3 - 4)

DMPV = -9000

DMPV = 9000 Adverse

The material price variance is adverse because the actual price is higher than the standard.

How many questions did you answer correctly?

Score Grade

4 Master

3 Pass