Direct Material Quantity Variance (DMQV) measures how efficiently a manufacturing business can convert its raw materials into the final product.

In this post, I will explain what the direct material quantity variance is, its causes, and the different ways you can calculate it using examples. Don’t forget to test your understanding by solving the free quiz at the end of the post!

Direct Material Quantity Variance

Direct Material Quantity Variance is the change in the cost of direct materials used in the manufacturing process arising from the difference between the actual quantity of materials used during a period, and the standard quantity of materials required to produce the actual output.

Direct Material Quantity Variance is also known as Direct Material Usage Variance and Direct Material Efficiency Variance.

How to Calculate Material Quantity Variance

To calculate the direct material quantity variance, we measure the difference between the standard cost of materials that should have been used to produce the actual level of output and the standard cost of the actual quantity of materials used.

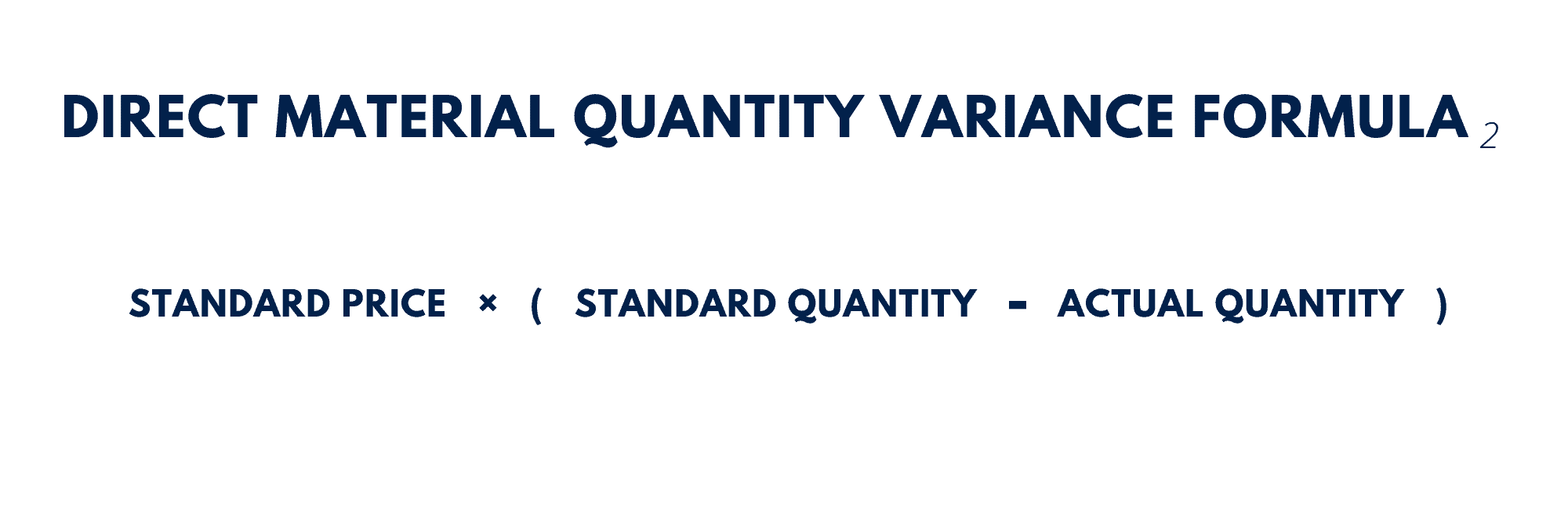

Another way to calculate the direct material quantity variance is to multiply the standard price of materials by the difference between the actual quantity of materials used in production and the standard quantity of materials that should have been used to produce the actual output.

You can calculate the standard quantity of materials by multiplying the standard quantity of materials per unit of output by the actual units of output produced in a given period.

Example

During a period, the Teddy Bear Company used 15,000 kilograms of stuffing material to produce 9000 teddy bears. The company had paid an average price of $1.5 per kilogram of stuffing material.

The materials budget for the same period allows 2 kilograms of stuffing material for each teddy bear at a standard price of $1 per kilogram.

Calculate the direct material quantity variance.

The first step in the calculation is to figure out how much stuffing material should be used to manufacture 9000 teddy bears (standard quantity).

Standard Quantity = Actual output × Standard usage per unit of output

= 9000 × 2

=18,000 KGs

Now that we know the standard quantity, we can use the DMQV formula to calculate the variance.

DMQV = Standard Quantity × Standard Price – Actual Quantity × Standard Price

DMQV = 18,000 × $1 – 15,000 × $1

DMQV = $18,000 – $15,000

DMQV = $3,000 Favorable

The material quantity variance in this example is favorable because the company manufactured the output using a lesser quantity of materials than what was planned in the budget.

We can also calculate the quantity variance using the second formula.

DMQV = Standard Price × ( Standard Quantity – Actual Quantity)

DMQV = $1 × ( 18,000 – 15,000 )

DMQV = $1 × 3,000

DMQV = $3,000 Favorable

You can check this video of mine for more examples of the material quantity variance.

Favorable Material Quantity Variance

Material quantity variance is favorable if the actual quantity of materials used in manufacturing during a period is lower than the standard quantity that was expected for that level of output.

In other words, if the business has consumed fewer materials to produce a given level of output than expected, the material quantity variance is said to be favorable.

Reasons for a favorable material quantity variance include:

- The use of bigger or better equipment to process the materials for reducing production losses.

- An improvement in the quality of materials purchased.

- More efficient use of materials by the production staff through better hiring, training, and gaining more experience.

- Optimizing the manufacturing process to lower the wastage of materials and frequency of breakdowns.

- Overestimating the materials usage in the budget.

Unfavorable Material Quantity Variance

An adverse or unfavorable material quantity variance occurs when the actual volume of materials used in production exceeds the standard quantity that is expected for the level of output in a period.

Causes for an adverse material quantity variance include:

- An increase in the frequency of equipment failures leading to a spike in production losses.

- The purchase of substandard materials that are difficult to work with or have a higher than usual percentage of defects.

- Inefficiencies in the manufacturing process (e.g., not recycling wastage).

- Turnover of experienced production staff.

- Underestimating the materials usage in the budget.

Question 1

DMQV = _________ Price × (Standard Quantity × Actual Quantity)

Actual

Incorrect.

Standard

Spot on!

Question 2

The direct material quantity variance will be adverse if the actual quantity of fabric used in manufacturing 10,000 units of shirts is 30,000 meters and the standard amount of fabric allowed for a single shirt is 2.8 meters.

True

Wrong answer.

False

You're right!

The MQV should be favorable because the standard quantity of the fabric for making 10,000 shirts is 28,000 meters which is less than what was actually used (30,000 meters).

Question 3

How many units of materials were used in the production if:

- The standard price of materials is $5 per unit.

- The actual output during the period is 1000 units.

- The standard quantity of materials is 2 liters per unit of output.

- The DMQV is $3000 adverse.

1400

liters

Wrong answer.

2000

liters

Incorrect.

2600

liters

That is correct!

DMQV = SP × (SQ - AQ)

-3000 = 5 × (2×1000 - AQ)

-3000 / 5 = 2000 - AQ

-600 = 2000 - AQ

-600 - 2000 = -AQ

AQ = 2600

3000

liters

Not correct.

Question 4

What is the direct material quantity variance if:

- The actual quantity of materials used is 200 units.

- The standard quantity of materials for 1 unit of output is 1 KG.

- The actual output is 250 units.

- The standard price of materials is $3 per KG.

- The actual price of materials of $5 per KG.

$250

Adverse

Incorrect.

$250

Adverse

Not correct.

$150

Favorable

Correct!

Standard Quantity = 250 × 1 = 250 KG

DMQV = SP × (SQ - AQ)

= $3 × (250 - 200)

=$150 Favorable

$150

Adverse

Incorrect.

How many questions did you answer correctly?

Score Grade

4 Master

3 Pass