To fully understand why we don’t depreciate land cost in accounting, let’s quickly recap why we even calculate depreciation in the first place.

Most long-lived assets are not expected to last forever in a business.

Assets like equipment, furniture, and vehicles typically have a useful life of three to twenty years before needing replacement. Buildings might last twenty to fifty years before needing significant renovations.

By the time such assets reach the end of their useful lives, they will usually be worth a lot less than their original cost because of obsolescence and physical deterioration.

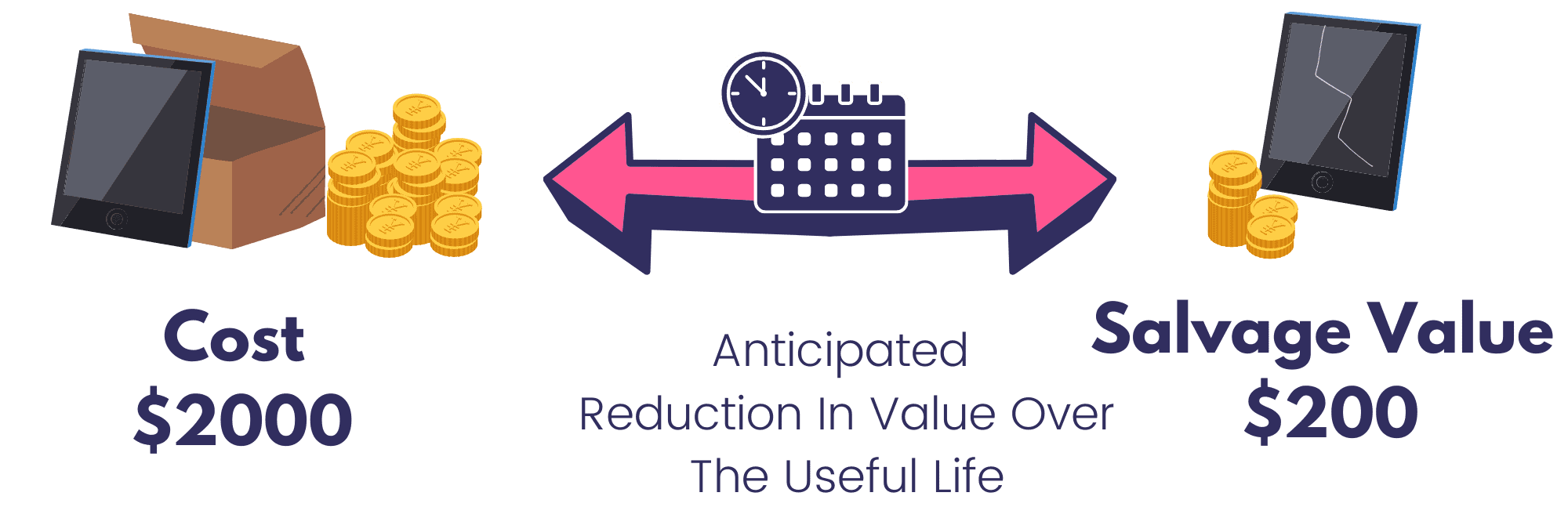

For example, a graphics tablet that costs $2000 to buy may be expected to last only 5 years at a web design agency before it becomes obsolete and needs to be replaced by newer models. Let’s say we expect the graphics tablet to sell for just $200 in 5 years’ time, this means that the cost to the business of using the asset for its entire useful life is estimated to be $1800 ($2000 initial cost minus $200 scrap value).

Instead of dumping the $1800 cost entirely in the first accounting period in which the asset is acquired or the last accounting period in which the asset will be sold, we split the cost and charge only a portion of it every year as a depreciation expense.

So the basic idea of calculating depreciation is to spread the anticipated reduction in the value of a long-term asset (which is $1800 in the example above) over its useful life (5 years). Using the straight-line basis in the example above, the depreciation charge for the graphics tablet would work out to be $360 for each year of the useful life ($1800 divided by 5).

Depreciation, therefore, gives a more accurate and predictable view of how profitable a business is from year to year because any income that is earned from using the long-term asset in a single accounting period gets matched by the proportional depreciation expense for that period.

Now, going back to our main question.