The most obvious connection between a balance sheet and an income statement is retained earnings. Whatever the business earns during an accounting period is accumulated as retained earnings in the balance sheet’s equity section.

However, there are also some less apparent links between the two reports that help to assign revenues and expenses to the correct accounting periods when the accrual basis of accounting is used.

The following diagram shows the different connections between the balance sheet and income statement prepared under the accrual basis.

- Under the accrual method, expenses and revenue are recorded in the income statement of the accounting period to which they relate to irrespective of when the cash flow occurs. As a result, several timing differences arise from the recognition of income/expenses and their cash flow that needs to be accounted for in the balance sheet in the form of accruals, inventory, receivables, prepayments, and payables.

- The cost of goods sold expense is calculated in the income statement by adding the amount of inventory reported in the balance sheet at the start of an accounting period, and subtracting its amount reported at the end of the period.

- Depreciation of fixed assets during an accounting period reduces the carrying value of fixed assets recognized in the balance sheet and also increases the amount of expenses reported in the income statement for that period.

- The difference between income and expenses (net income) reported in the income statement is added to the retained earnings under the balance sheet’s equity section.

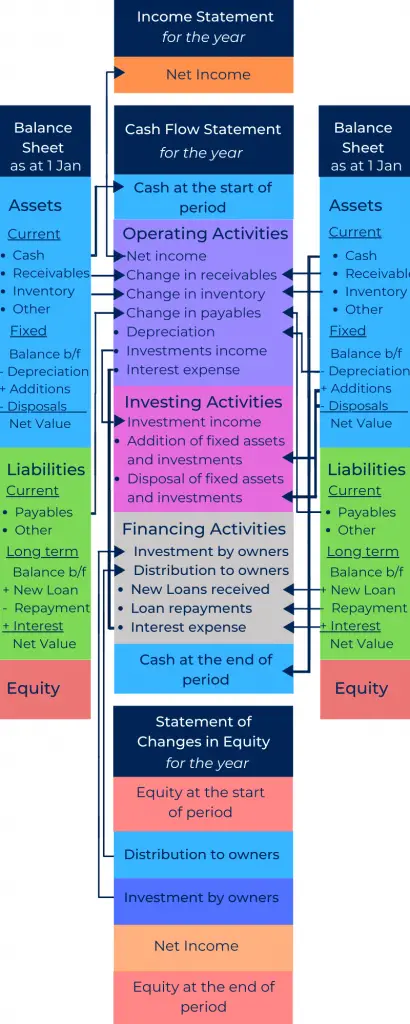

The statement of cash flows explains the sources of inflows and outflows of a business’s monetary resources over the accounting period.

- The total cash flow reported in the cash flow statement is equal to the difference between the cash presented in the balance sheet at the start and end of an accounting period.

- Cash flow from operating activities is the cash generated from the transactions reported in the income statement.

- When the accruals basis of accounting is used, the net income will not equal the cash flow from operations. As a result, the following adjustments are required to calculate the cash flow from operations from the net income of that period:

- Adding back non-cash expenses such as depreciation as they do not involve any cash flow.

- Changes in receivables, payables, and inventory (working capital) reported in the balance sheet at the start and end of the accounting period. This removes the effect of income and expenses that have not yet resulted in cash flow.

- Exclusion of any income or expense reported in the income statement that ought to be shown elsewhere in the cash flow statement, such as interest expense, which is classified under financing activities.

- Cash flow from investing activities includes any income from investments that appear in the income statement. This section also includes the changes in cash flow arising from the purchase and disposal of long term assets and investments.

- Investments by owners and any distributions to them are shown under the financing activities section of the cash flow statement. These amounts can be traced back to the statement of changes in equity.

- Cash flow from financing activities also consists of loan receipts, interest cost and principal repayment of loans made during an accounting period.

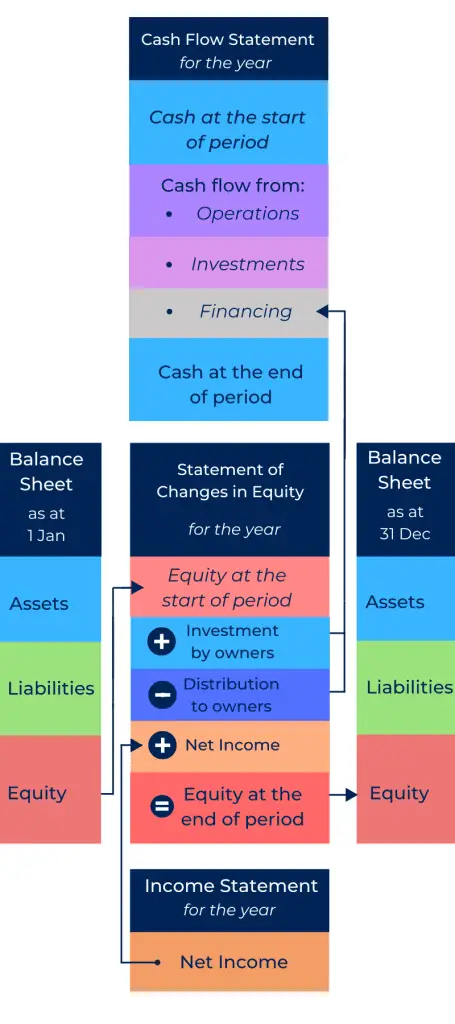

As the name implies, the statement of changes in equity shows the changes to the owners’ equity presented in the balance sheet over an accounting period.

- The net income (profit or loss) reported in the income statement is accumulated in the retained earnings account presented in the balance sheet’s equity section.

- Investment by owners, such as by the issuance of share capital, is added to the owners’ equity.

- Any distributions made to business owners, such as dividend payments, are deducted from the amount of equity.

- Investments from and distributions to owners are shown in the cash flow statement under the heading of financial activities.

- Any gains and losses (e.g., revaluation gains) that are recognized outside of the income statement also appear in this report.

- The closing total of the statement of changes in equity equals to the total equity reported in the balance sheet at the end of the accounting period.